[et_pb_section admin_label=”Header – All Pages” global_module=”1221″ transparent_background=”off” background_color=”#1e73be” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”||0px|”][et_pb_row global_parent=”1221″ admin_label=”row”][et_pb_column type=”4_4″][et_pb_post_title global_parent=”1221″ admin_label=”Post Title” title=”on” meta=”off” author=”on” date=”on” categories=”on” comments=”on” featured_image=”off” featured_placement=”below” parallax_effect=”on” parallax_method=”on” text_orientation=”left” text_color=”light” text_background=”off” text_bg_color=”rgba(255,255,255,0.9)” module_bg_color=”rgba(255,255,255,0)” title_all_caps=”off” use_border_color=”off” border_color=”#ffffff” border_style=”solid” title_font=”|on|||” title_font_size=”35″ custom_padding=”10px|||”] [/et_pb_post_title][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” global_module=”1228″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” custom_padding=”0px||0px|” padding_mobile=”on” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row global_parent=”1228″ admin_label=”Row” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”0px||0px|” padding_mobile=”off” allow_player_pause=”off” parallax=”off” parallax_method=”off” make_equal=”off” parallax_1=”off” parallax_method_1=”off” column_padding_mobile=”on”][et_pb_column type=”4_4″][et_pb_text global_parent=”1228″ admin_label=”Text” background_layout=”light” text_orientation=”left” text_font_size=”14″ use_border_color=”off” border_color=”#ffffff” border_style=”solid”]

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” fullwidth=”off” specialty=”off”][et_pb_row admin_label=”Row”][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” text_font_size=”14″ use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”http://www.frs102.com/members/premium-toolkit/” type=”big” color=”red”] Return to Main Index[/button] [/et_pb_text][/et_pb_column][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” text_font_size=”14″ use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”http://frs102.com/members/premium-toolkit/section-11/” type=”big” color=”red”] Return to Section 11 Home[/button] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row admin_label=”Row”][et_pb_column type=”4_4″][et_pb_text admin_label=”Main Body Text” background_layout=”light” text_orientation=”justified” use_border_color=”off” border_color=”#ffffff” border_style=”solid”]Impairments of financial assets held at cost or amortised cost

Extract from FRS 102 Section 11.21-11.26

Recognition

11.21 At the end of each reporting period, an entity shall assess whether there is objective evidence of impairment of any financial assets that are measured at cost or amortised cost. If there is objective evidence of impairment, the entity shall recognise an impairment loss in profit or loss immediately.

11.22 Objective evidence that a financial asset or group of assets is impaired includes observable data that come to the attention of the holder of the asset about the following loss events:

(a) significant financial difficulty of the issuer or obligor;

(b) a breach of contract, such as a default or delinquency in interest or principal payments;

(c) the creditor, for economic or legal reasons relating to the debtor’s financial difficulty, granting to the debtor a concession that the creditor would not otherwise consider;

(d) it has become probable that the debtor will enter bankruptcy or other financial reorganisation; and

(e) observable data indicating that there has been a measurable decrease in the estimated future cash flows from a group of financial assets since the initial recognition of those assets, even though the decrease cannot yet be identified with the individual financial assets in the group, such as adverse national or local economic conditions or adverse changes in industry conditions

11.23 Other factors may also be evidence of impairment, including significant changes with an adverse effect that have taken place in the technological, market, economic or legal environment in which the issuer operates.

11.24 An entity shall assess the following financial assets individually for impairment:

(a) all equity instruments regardless of significance; and

(b) other financial assets that are individually significant.

An entity shall assess other financial assets for impairment either individually or grouped on the basis of similar credit risk characteristics.

Measurement

11.25 An entity shall measure an impairment loss on the following instruments measured at cost or amortised cost as follows:

(a) For an instrument measured at amortised cost in accordance with paragraph 11.14(a), the impairment loss is the difference between the asset’s carrying amount and the present value of estimated cash flows discounted at the asset’s original effective interest rate. If such a financial instrument has a variable interest rate, the discount rate for measuring any impairment loss is the current effective interest rate determined under the contract.

(b) For an instrument measured at cost less impairment in accordance with paragraph 11.14(c) and (d)(ii) the impairment loss is the difference between the asset’s carrying amount and the best estimate (which will necessarily be an approximation) of the amount (which might be zero) that the entity would receive for the asset if it were to be sold at the reporting date.

Reversal

11.26 If, in a subsequent period, the amount of an impairment loss decreases and the 11.23 Other factors may also be evidence of impairment, including significant changes with an adverse effect that have taken place in the technological, market, economic or legal environment in which the issuer operates.

OmniPro comment

Impairment of financial assets is only relevant to assets measured at amortised cost or cost. For financial assets which are held at fair value, the diminuation is recognised year on year as it is carried at fair value. At the end of each reporting period an entity is required to assess whether there are indicators/objective evidence of impairment of financial assets and if there is an impairment should be booked. Detailed in Section 11.22 and 11.23 above are the detailed impairment indicators. They are summarised as follows:

(a) significant financial difficulty of the issuer or obligor;

(b) a breach of contract, such as a default or delinquency in interest or principal payments;

(c) the creditor, for economic or legal reasons relating to the debtor’s financial difficulty, granting to the debtor a concession that the creditor would not otherwise consider;

(d) it has become probable that the debtor will enter bankruptcy or other financial reorganisation; and

(e) observable data indicating that there has been a measurable decrease in the estimated future cash flows from a group of financial assets since the initial recognition of those assets, even though the decrease cannot yet be identified with the individual financial assets in the group, such as adverse national or local economic conditions or adverse changes in industry conditions;

(f) other factors may also be evidence of impairment, including significant changes with an adverse effect that have taken place in the technological, market, economic or legal environment in which the issuer operates;

(h) the solvency, business and financial risk exposures of the debtor;

(i) levels of, and trends in, delinquencies for similar financial assets;

(j) A downgrade in the entity’s credit rating.

The standard requires that all ordinary and preference shares are assessed for impairment individually. Other financial assets can be grouped where it is determined appropriately and can usually be done on a collective basis where it is performed on the basis of credit risks.

Impairment debt instruments

For debt instruments which have a fixed rate which are measured at amortised cost, the difference between the asset’s carrying amount and the present value of estimated cash flows discounted at the asset’s original effective interest rate when it was initially recognised.

For variable debt instruments, the discount rate to be used is the current effective interest rate determined under the contract. For example, if the debt instrument was issued at LIBOR + 50 basis points. The LIBOR rate at initial recognition was 3%, but the LIBOR rate at the date of the impairment indicator is 5%. The 5% is used as part of the impairment review as the LIBOR was stated in the contract.

Where an impairment is identified a provision can be booked against the impairment or the amount can be written off.

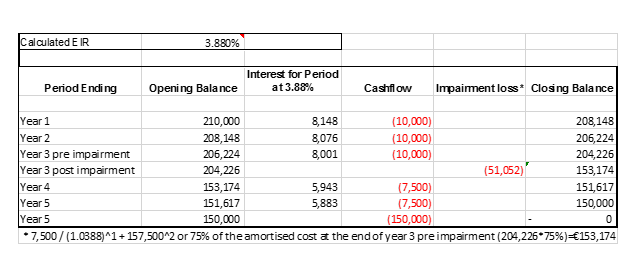

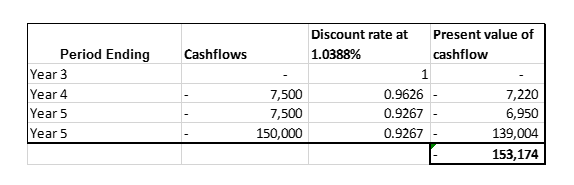

Example 20: Impairment of debt instruments

Company A issued a loan to a related company for CU200,000 and incurred costs of CU10,000 at the start of year 1 for 5 years. Interest at a fixed rate of 5% was charged (i.e. CU10,000 per annum) which was deemed to be the market rate of the loan at that date. At the end of year 3 the related company’s financial performance deteriorated and shows signs that the full amount will not be recoverable. Company A estimates that it will only receive 75% of the interest (i.e. CU150,000*5%=CU7,500) and 75% of the capital (i.e. CU200,000*75%=CU150,000). Therefore, an impairment loss is required to be booked. The effective rate on taking out the loan was 3.88% which was calculated using a mathematical model in Excel.

NOTE: if in the above example the entity determined there to be doubt about the recoverability of the full asset an impairment of CU204,202 would be booked.

If the impairment review reverses in a prior period, then the impairment can be reversed to the P&L. Any reversal of a prior year impairment cannot reinstate the amortised cost above that what it would have been if no impairment was required.

Impairment of financial assets carried at cost

This applies to ordinary or preference shares which are not publically traded and whose fair value cannot be reliably measured. Where there is objective evidence that a loss has occurred then the amount of the impairment is the difference between the asset’s carrying amount and the best estimate of the amount the entity would receive on a sale at that reporting date.

Extract from FRS 102 Section 11.33-11.3

11.33 An entity shall derecognise a financial asset only when:

(a) the contractual rights to the cash flows from the financial asset expire or are settled; or

(b) the entity transfers to another party substantially all of the risks and rewards of ownership of the financial asset; or

(c) the entity, despite having retained some significant risks and rewards of ownership, has transferred control of the asset to another party and the other party has the practical ability to sell the asset in its entirety to an unrelated third party and is able to exercise that ability unilaterally and without needing to impose additional restrictions on the transfer. In this case, the entity shall:

(i) derecognise the asset; and

(ii) recognise separately any rights and obligations retained or created in the transfer.

The carrying amount of the transferred asset shall be allocated between the rights or obligations retained and those transferred on the basis of their relative fair values at the transfer date. Newly created rights and obligations shall be measured at their fair values at that date. Any difference between the consideration received and the amounts recognised and derecognised in accordance with this paragraph shall be recognised in profit or loss in the period of the transfer.

11.34 If a transfer does not result in derecognition because the entity has retained significant risks and rewards of ownership of the transferred asset, the entity shall continue to recognise the transferred asset in its entirety and shall recognise a financial liability for the consideration received. The asset and liability shall not be offset. In subsequent periods, the entity shall recognise any income on the transferred asset and any expense incurred on the financial liability.

11.35 If a transferor provides non-cash collateral (such as debt or equity instruments) to the transferee, the accounting for the collateral by the transferor and the transferee depends on whether the transferee has the right to sell or repledge the collateral and on whether the transferor has defaulted. The transferor and transferee shall account for the collateral as follows:

(a) If the transferee has the right by contract or custom to sell or repledge the collateral, the transferor shall reclassify that asset in its statement of financial position (e.g. as a loaned asset, pledged equity instruments or repurchase receivable) separately from other assets.

(b) If the transferee sells collateral pledged to it, it shall recognise the proceeds from the sale and a liability measured at fair value for its obligation to return the collateral.

(c) If the transferor defaults under the terms of the contract and is no longer entitled to redeem the collateral, it shall derecognise the collateral, and the transferee shall recognise the collateral as its asset initially measured at fair value or, if it has already sold the collateral, derecognise its obligation to return the collateral.

(d) Except as provided in (c), the transferor shall continue to carry the collateral as its asset, and the transferee shall not recognise the collateral as an asset.

OmniPro comment

In Section 11.33 (a), a financial asset can be derecognised if the asset is settled or expires.

Example 21: asset recognised due to settlement

Company A loans CU100,000 to another entity which attracted a market interest rate and was repayable in year 5.

The asset can be derecognised at the end of year 5 i.e. when the loan is fully repaid. If the loan is repaid earlier then it is derecognised on the date it is repaid.

In Section 11.33 (b), a financial asset can be derecognised when the entity transfers to another party substantially all of the risks and rewards of ownership of the financial asset.

Example 22: sale of debtors with recourse

Company A arranges invoice discounting with a bank. They sell their book of debtors which is stated at CU200,000 for CU180,000. However the company retains the credit risk. The company manages the debtors book and pays over any receipts to the bank. Given that substantially all the risk and rewards of ownership have not been transferred, as Company A will incur any bad debt risk, the debtor balance cannot be derecognised. As a result the way in which this CU180,000 is recognised is to:

|

|

CU |

CU |

|

Debit bank account |

180,000 |

|

|

Credit invoice discounting liability |

|

180,000 |

NOTE: the interest charged by the bank is charged to the P&L as incurred and any transaction costs are released over the life of the arrangement such that the liability is held at amortised cost.

Example 23: sale of debtors with recourse

Company A arranges invoice discounting with a bank. They sell their book of debtors which is stated at CU200,000 for CU180,000. The bank also takes on the credit risk. The company manages the debtors book and pays over any receipts to the bank. Given that substantially all the risk and rewards of ownership have been transferred, the company can derecognise the trade debtor balance. The journal to derecognise this is to:

|

|

CU |

CU |

|

Dr Bank Account |

180,000 |

|

|

Dr Profit and Loss – Bank Charges |

20,000 |

|

|

Cr Trade Debtors |

|

200,000 |

In Section 11.33 (c), a financial asset can be derecognised when the entity, despite having retained some significant risks and rewards of ownership, has transferred control of the asset to another party and the other party has the practical ability to sell the asset in its entirety. These are the key requirements.

Example 24: Transfer of assets at fair value subject to a call option

Company A owned publically quoted shares with a fair value of CU50,000. The company decided to sell these shares for CU45,000 to a bank with an option to purchase these in 6 months for CU55,000.

It is noted that the risk and rewards of ownership have not been substantially transferred as Company A has an option to purchase the shares back if the value of the shares is above CU55,000. However, given that the bank can sell the shares themselves in an active market and then repurchase them at a later date if the option is called in, it therefore means that the bank has control as it meets the definition in Section 11.33 (c). On this basis as control has passed, the asset can be derecognised. The journals to be posted are as follows:

|

|

CU |

CU |

|

Dr Bank Account |

45,000 |

|

|

Cr Investments |

|

50,000 |

|

Cr fair value of Call option (to be accounted for under Section 12) |

|

5,000 |

Note there has to be an ability for the other party to dispose of the asset to another party. This would not be the case for a debtor’s book balance where credit risk was maintained by Company A.

As detailed in 11.35, where non cash collateral is provided (e.g. in the form of shares or debt) it needs to be separated and disclosed in the financial statements, however it is not derecognised until the entity defaults on any loan.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]