[et_pb_section admin_label=”Header – All Pages” global_module=”1221″ transparent_background=”off” background_color=”#1e73be” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”||0px|”][et_pb_row global_parent=”1221″ admin_label=”row”][et_pb_column type=”4_4″][et_pb_post_title global_parent=”1221″ admin_label=”Post Title” title=”on” meta=”off” author=”on” date=”on” categories=”on” comments=”on” featured_image=”off” featured_placement=”below” parallax_effect=”on” parallax_method=”on” text_orientation=”left” text_color=”light” text_background=”off” text_bg_color=”rgba(255,255,255,0.9)” module_bg_color=”rgba(255,255,255,0)” title_all_caps=”off” use_border_color=”off” border_color=”#ffffff” border_style=”solid” title_font=”|on|||” title_font_size=”35″ custom_padding=”10px|||”] [/et_pb_post_title][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” global_module=”1228″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” custom_padding=”0px||0px|” padding_mobile=”on” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row global_parent=”1228″ admin_label=”Row” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”0px||0px|” padding_mobile=”off” allow_player_pause=”off” parallax=”off” parallax_method=”off” make_equal=”off” parallax_1=”off” parallax_method_1=”off” column_padding_mobile=”on”][et_pb_column type=”4_4″][et_pb_text global_parent=”1228″ admin_label=”Text” background_layout=”light” text_orientation=”left” text_font_size=”14″ use_border_color=”off” border_color=”#ffffff” border_style=”solid”]

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” fullwidth=”off” specialty=”off”][et_pb_row admin_label=”Row”][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” text_font_size=”14″ use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”http://www.frs102.com/members/premium-toolkit/” type=”big” color=”red”] Return to Main Index[/button] [/et_pb_text][/et_pb_column][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” text_font_size=”14″ use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”http://frs102.com/members/premium-toolkit/section-11/” type=”big” color=”red”] Return to Section 11 Home[/button] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row admin_label=”Row”][et_pb_column type=”4_4″][et_pb_text admin_label=”Main Body Text” background_layout=”light” text_orientation=”justified” use_border_color=”off” border_color=”#ffffff” border_style=”solid”]Derecognition of financial liabilities

Extract from FRS 102 Section 11.36-11.38

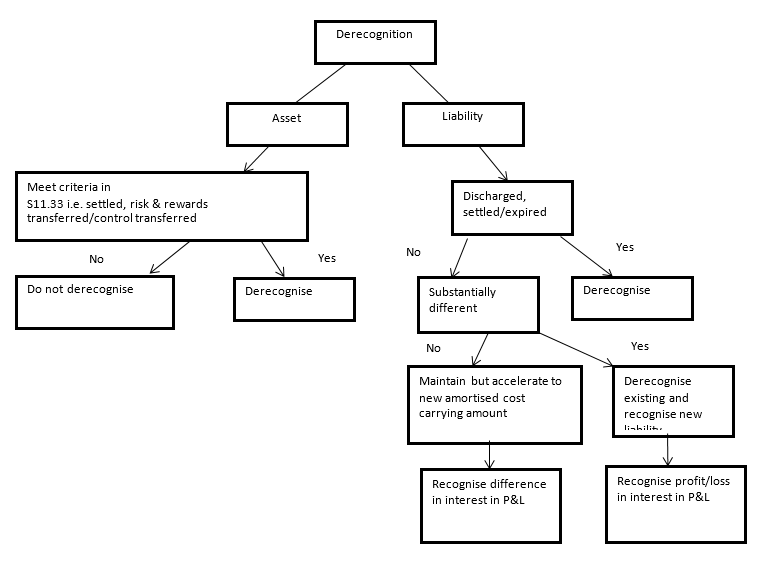

11.36 An entity shall derecognise a financial liability (or a part of a financial liability) only when it is extinguished i.e. when the obligation specified in the contract is discharged, is cancelled or expires.

11.37 If an existing borrower and lender exchange financial instruments with substantially different terms, the entities shall account for the transaction as an extinguishment of the original financial liability and the recognition of a new financial liability. Similarly, an entity shall account for a substantial modification of the terms of an existing financial liability or a part of it (whether or not attributable to the financial difficulty of the debtor) as an extinguishment of the original financial liability and the recognition of a new financial liability.

11.38 The entity shall recognise in profit or loss any difference between the carrying amount of the financial liability (or part of a financial liability) extinguished or transferred to another party and the consideration paid, including any non-cash assets transferred or liabilities assumed.

OmniPro comment

In its simplest terms, a liability is extinguished once a loan is repaid in full or the entity has been released from the obligation by the creditor.

However there are instances where it is not as simple to determine whether a liability is extinguished or if in fact it has just been modified. The standard merely states that a substantial modification should be treated as an extinguishment. It does not provide detail on how to account for a modification which is not considered substantial i.e. how to account for the difference between the present value of the modified cash flows discounted at the original effective interest rate and the carrying amount of the debt instrument at that date. There is a choice as to how this difference should be accounted for as detailed in example 26 to either:

- Recognise the difference in the profit and loss account to accelerate the charge/income (as shown in example 14 above); or

- Charge the interest over a new effective interest rate such that the carrying value at the end of the term equates to the actual capital amount. Where fees are incurred these would be netted against the present value of the future cash flows and amortised over the remaining life of the debt instrument.

Neither does it define what the meaning of a substantial modification is. Some qualitative examples which can help in an assessment as to whether there is a substantial modification are:

- A change in interest rate from fixed to floating, or vice versa

- Material difference between the maturity date before the modification and after the modification.

- Material changes in covenants and conversion terms between the old and new debt.

The above are only qualitative factors. IAS 39 of IFRS provides a quantitative guideline as to what should be considered to be a substantial modification. IFRS outlines that a substantial change arises where the discounted present value of the cash flows under the new terms, including any fees paid, net of any fees received discounted using the original effective interest rate is at least 10% different from the discounted present value of the remaining cash flows of the original financial liability. Although this is not specifically stated in Section 11, it appears reasonable that such a basis be used as a difference of 10% would be substantial. See example below

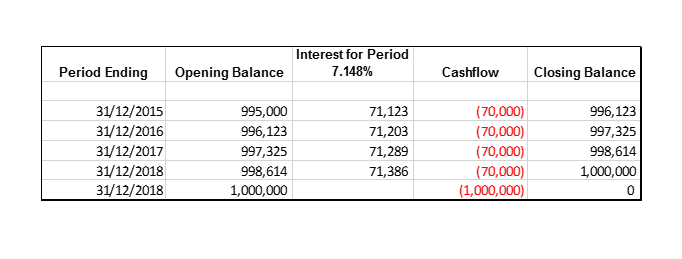

Example 25: Substantial modification of a loan

Company A took out a loan for CU1,000,000 on 01/01/15 with a bank which was due to be repaid on 31/12/18. Interest was charged at a rate of 7% (CU70,000 per annum) and arrangement fees of CU5,000. Due to poor trading conditions at 31/12/16, the company renegotiated the facility with the bank. The revised terms are as follows:

- loan is now repayable on 31/12/22

- Interest – 6.25% (6.25%*CU800,000= CU50,000)

- Maturity – 31/12/23

- Final principal due on maturity of CU800,000

- Cost of renegotiation of CU4,000

Should the above be treated as a modification of an existing loan or an extinguishment of an existing loan and its replacement by a new loan?

Step 1: Amortise old facility up to date of the modification. The effective interest rate has been determined through the use of Excel.

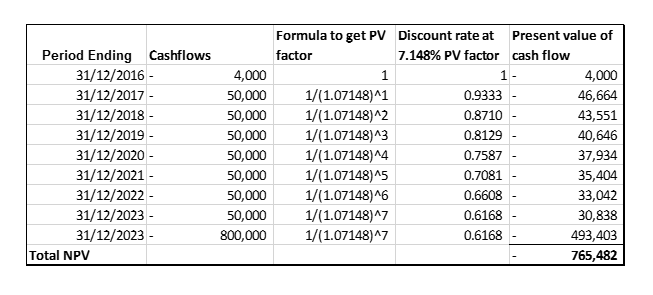

Step 2: Calculate present value of future estimated cash flows under revised terms discounted at original EIR of 7.148%

Determine if a substantial modification has occurred i.e. is the modification 10% or more

Extent of modification = A – B = (CU997,325-CU765,482) = 23.2% A CU997,325

Where A = The present value of remaining cash flows under original terms using original EIR = CU997,325

Where B = The present value of revised cash flows using original EIR of CU765,482

As the difference of CU231,843 (CU997,325-CU765,482) is greater than 10%, this is treated as an extinguishment. Therefore, the journal required to derecognise are:

|

|

CU |

CU |

|

Debit Financial Liability |

997,325 |

|

|

Dr Interest Expense |

2,675 |

|

|

Cr Cash |

|

1,000,000 |

In effect what gets written off to the P&L is the unamortised element of the initial arrangement fee of CU5,000.

The fair value of the new financial liability would then be recognised, the fair value could be obtained by discounting the cash flows of the modified loan at the interest rate at which the company could have obtained this new loan at in the market. If we assume the fair value of the new loan is CU999,000, the accounting journals would be:

|

|

CU |

CU |

|

Dr Cash |

1,000,000 |

|

|

Cr Financial Liability |

|

999,000 |

|

Cr Interest Expense |

|

1,000 |

If the above was not above 10% and therefore was not deemed to be a substantial modification, there is a choice as to how to account for the unamortised expenses. The unamortised expenses can be amortised over the remaining life of the negotiated instrument net of any associated fees (can be on a straight line basis or a revised EIR basis so as to allow the unamortised element to come to the capital value at the end of its life e.g. in the example above the CU993,325 (CU997,325-CU4,000 fees) would be amortised such that the capital amount comes to CU800,000 by the end of 2023) or as would be done for a change in estimated cash flows, the current carrying amount is adjusted to reflect the revised present value of estimated cash flows and the remaining amount amortised over the original effective rate of interest (See example 13a for example of same).

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]