[et_pb_section bb_built=”1″ admin_label=”Header – All Pages” transparent_background=”off” background_color=”#1e73be” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”||0px|” next_background_color=”#ffffff” custom_padding_tablet=”50px|0|50px|0″ custom_padding_last_edited=”on|desktop” global_module=”1221″][et_pb_row admin_label=”row” global_parent=”1221″ background_position=”top_left” background_repeat=”repeat” background_size=”initial”][et_pb_column type=”4_4″][et_pb_post_title global_parent=”1221″ title=”on” meta=”off” author=”on” date=”on” categories=”on” comments=”on” featured_image=”off” featured_placement=”below” parallax_effect=”on” parallax_method=”off” text_orientation=”left” text_color=”light” text_background=”off” text_bg_color=”rgba(255,255,255,0.9)” module_bg_color=”rgba(255,255,255,0)” title_all_caps=”off” use_border_color=”off” border_color=”#ffffff” border_style=”solid” title_font=”|on|||” title_font_size=”35″ custom_padding=”10px|||” parallax=”on” background_color=”rgba(255,255,255,0)” /][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” custom_padding=”0px||0px|” padding_mobile=”on” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ prev_background_color=”#1e73be” next_background_color=”#ffffff” custom_padding_tablet=”0px||0px|” global_module=”1228″][et_pb_row global_parent=”1228″ make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”0px||0px|” padding_mobile=”off” allow_player_pause=”off” parallax=”off” parallax_method=”off” make_equal=”off” parallax_1=”off” parallax_method_1=”off” column_padding_mobile=”on” background_position=”top_left” background_repeat=”repeat” background_size=”initial”][et_pb_column type=”4_4″][et_pb_text global_parent=”1228″ background_layout=”light” text_orientation=”left” text_font_size=”14″ use_border_color=”off” border_color=”#ffffff” border_style=”solid” background_position=”top_left” background_repeat=”repeat” background_size=”initial”]

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section bb_built=”1″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ custom_padding_tablet=”50px|0|50px|0″ custom_padding_last_edited=”on|desktop” prev_background_color=”#ffffff” next_background_color=”#000000″][et_pb_row background_position=”top_left” background_repeat=”repeat” background_size=”initial”][et_pb_column type=”4_4″][et_pb_toggle admin_label=”Index” _builder_version=”3.0.106″ title=”Index” open=”off”]Contents

34.2 Agriculture – recognition and measurement.

34.2.1 Extract from FRS102: Section 34.2-.34.3B.

34.2.2.1 The meaning of biological assets and examples.

34.2.2.1.1 Agricultural activity defined.

34.2.2.1.1.1 Requirements for biological transformation.

34.2.2.1.1.2 Requirements for biological transformation to be managed.

34.2.2.1.2 Biological asset defined.

34.2.2.2 Recognition criteria.

34.2.2.3 Accounting for agricultural produce within the scope of Section 34.

34.2.2.4 Items excluded from the definition of agriculture.

34.2.2.5 Accounting policy choices:

34.2.2.5.3 Accounting policy choice by class.

34.2.2.6 Accounting for agricultural produce after point of harvest.

34.3 Measurement – fair value model.

34.3.1 Extract from FRS102: Section 34.4-.34.6A.

34.3.2.1 Initial and subsequent recognition.

34.3.2.2. Fair value hierarchy model.

34.3.2.2.1 Active market defined.

34.3.2.2.1.1. What market to use where there is more than one market and markets in other locations.

34.3.2.2.1.1.1 More than one market to sell the produce.

34.3.2.2.1.1.2 Market in different locations.

34.3.2.2.1.1.3 Use of cash flow model to determine fair value.

34.3.2.3 Application of the fair value model.

34.3.2.4 Fair values cannot be reliably measured.

34.5 Disclosures – fair value model.

34.5.1 Extract from FRS102: Section 34.7-34.7B.

34.5.2.2.1 Extract from accounting policies note for forestry.

34.5.2.2.2 Extract from accounting policies note for livestock (Extracted from Appendix to IAS 41).

34.5.2.3 Critical accounting estimates and judgments disclosure.

34.5.2.4 Notes to financial statements.

34.7 Measurement – cost model.

34.7.1 Extract from FRS102: Section 34.8-34.9.

34.7.2.1 Initial and subsequent measurement/

34.7.2.2 Choices when applying the cost model to agricultural produce.

34.8 Disclosures – cost model.

34.8.1 Extract from FRS102: Section 34.10-34.9.

34.8.2.3 Notes to the financial statements.

34.9.1 Extract from FRS102: Section 34.11-.34.11C.

34.10 Service Concession Arrangements.

34.10.1 Extract from FRS102: Section 34.12-.34.16A.

34.10.2.2 Service conditions arrangements defined.

34.10.2.2.1 Conditions that must apply.

34.11.1 Extract from FRS102: Section 34.17-.34.33.

34.11.2.2 Financial institution defined.

34.12 Retirement Benefit Plans: Financial Statements.

34.12.1 Extract from FRS102: Section 34.34-.34.48.

34.12.2.2 Full set of financial statements.

34.13.1 Extract from FRS102: Section 34.49-.34.56.

34.13.2.1 Heritage asset – defined.

34.13.2.2 Recognition and measurement.

34.13.2.3 What about old heritage assets where there are no records to determine cost.

34.13.2.4 Where should heritage assets be disclosed on the balance sheet.

34.13.2.5.1 Possible reasons for impairment.

34.13.2.6 Useful life and residual value.

34.13.2.7 Heritage assets received free of charge.

34.13.2.8.2 Illustration of some of the disclosure requirements for heritage assets.

34.14.1 Extract from FRS102: Section 34.57-.34.63 and Appendix A to Section 34.

34.15 Public benefit entities: Incoming Resources from Non-Exchange Transactions.

34.15.1 Extract from FRS102: Section PBE34.64-.PBE34.74 and Appendix B to Section 34.

34.15.2.1 Public benefit entity defined.

34.15.2.1.1 Requirement to disclose that an entity is a public benefit entity.

34.15.2.2 Special rules for public benefit entities.

34.15.2.2.1 Assets held for provision of social benefits.

34.15.2.2.2 Income resources from non-exchange transactions.

34.15.2.2.2.2 Accounting for non-exchange accounting.

34.15.2.2.2.2.1 Recognition for goods and measurement for goods.

34.15.2.2.2.2.1.1 Performance related conditions defined.

34.15.2.2.2.2.1.2 Conditions that are not performance related.

34.15.2.2.2.2.1.3 Examples of non-exchange resource transactions received in the form of goods.

34.15.2.2.2.2.2 Non-exchange resources received in the form of services/facilities.

34.15.2.2.2.2.2.2 Recognition and measurement.

34.15.2.2.2.2.2.2.1 Examples of non-exchange Transactions where services/facilities provided.

34.15.2.2.3 Public benefit entity combinations.

34.15.2.2.3.1.1 Business combinations defined.

34.15.2.2.3.2 Accounting Requirements.

34.15.2.2.3.2.1 Gift of a business for nil or nominal consideration.

34.15.2.2.3.2.1.1 Example of business combinations which is a gift that is not a merger.

34.15.2.2.3.2.1.2 Disclosures.

34.15.2.2.3.2.2 Examples illustrating merger accounting.

34.15.2.2.3.2.3 Meets the definition of a true acquisition and the purchase method applies.

34.15.2.2.3.2.3.1 Example business combination: Not a merger or gift – Purchase accounting method.

34.15.2.2.4 Public benefit concessionary loans.

34.15.2.2.4.2 Public benefit entity loan defined.

34.15.2.2.4.3 Accounting treatment of public benefit concessionary loans choices. 4

34.15.2.2.4.5 Examples of concessionary loans.

34.15.2.2.5 Government grants and accounting requirements.

34.15.2.2.5.1.1 Grants of all natures – Performance model.

34.15.2.2.5.1.2 Accrual model FRS 102 only.

34.15.2.2.5.2 Example of government grant accounting of PBE’S.

[/et_pb_toggle][/et_pb_column][/et_pb_row][et_pb_row][et_pb_column type=”3_4″][et_pb_text admin_label=”Main Body Text” background_layout=”light” text_orientation=”justified” use_border_color=”off” background_position=”top_left” background_repeat=”repeat” background_size=”initial” _builder_version=”3.0.106″]

34.15 Public benefit entities: Incoming Resources from Non-Exchange Transactions

34.15.1 Extract from FRS102: Section PBE34.64-.PBE34.74 and Appendix B to Section 34

PBE34.64 The accounting for government grants is addressed in Section 24 Government Grants.

PBE34.65 Paragraphs PBE34.67 to PBE34.74 and the accompanying guidance at Appendix B to this section apply to other resources received from non-exchange transactions by public benefit entities or entities within a public benefit entity group. A non-exchange transaction is a transaction whereby an entity receives value from another entity without directly giving approximately equal value in exchange or gives value to another entity without directly receiving approximately equal value in exchange.

PBE34.66 Non-exchange transactions include, but are not limited to, donations (of cash, goods, and services) and legacies

Recognition and measurement

PBE34.67 An entity shall recognise receipts of resources from non-exchange transactions as follows:

(a) Transactions that do not impose specified future performance-related conditions on the recipient are recognised in income when the resources are received or receivable.

(b) Transactions that do impose specified future performance-related conditions on the recipient are recognised in income only when the performance-related conditions are met.

(c) Where resources are received before the revenue recognition criteria are satisfied, a liability is recognised.

PBE34.68 The existence of a restriction does not prohibit a resource from being recognised in income when receivable.

PBE34.69 When applying the requirements of paragraph PBE34.67, an entity must take into consideration whether the resource can be measured reliably and whether the benefits of recognising the resource outweigh the costs.

PBE34.70 Therefore, where it is not practicable to estimate the value of the resource with sufficient reliability, the income shall be included in the financial period when the resource is sold.

PBE34.71 An entity shall recognise a liability for any resource that has previously been received and recognised in income when, as a result of a subsequent failure to meet restrictions or performance-related conditions attached to it, repayment becomes probable.

PBE34.72 Donations of services that can be reasonably quantified will usually result in the recognition of income and an expense. An asset will be recognised only when those services are used for the production of an asset and the services received will be capitalised as part of the cost of that asset.

PBE34.73 An entity shall measure incoming resources from non-exchange transactions as follows:

(a) Donated services and facilities that would otherwise have been purchased, shall be measured at the value to the entity.

(b) All other incoming resources from non-exchange transactions shall be measured at the fair value of the resources received or receivable.

Disclosure

PBE34.74 An entity shall disclose the following:

(a) the nature and amounts of resources receivable from non-exchange transactions recognised in the financial statements;

(b) any unfulfilled conditions or other contingencies attaching to resources from non-exchange transactions that have not been recognised in income; and

(c) an indication of other forms of resources from non-exchange transactions from which the entity has benefited.

Appendix B to Section 34

Guidance on incoming resources from non-exchange transactions (paragraphs 34.64 to 34.74)

This guidance is an integral part of the Standard.

Recognition

PBE34B.1 The receipt of resources will usually result in an entity recognising an asset and corresponding income for the fair value of resources when those resources become received or receivable. Instances when this may differ include where:

(a) an entity received those resources in the form of services (see paragraphs PBE34B.8 to PBE34B.12); or

(b) there are performance-related conditions attached to the resources, which have yet to be fulfilled (see paragraphs PBE34B.13 to PBE34B.14).

PBE34B.2 Resources shall only be recognised when the fair value of the incoming resources can be measured reliably.

PBE34B.3 The concepts of materiality (see paragraph 2.6), and balance between benefit and cost (see paragraph 2.13) should be considered when deciding which resources received shall be recognised in the financial statements.

PBE34B.4 When it is impracticable to recognise resources from non-exchange transactions, the income is recognised in the period in which the resources are sold or distributed. The most common example is that of high volume, low value second-hand goods donated for resale.

Legacies

PBE34B.5 Donations in the form of legacies are recognised when it is probable that the legacy will be received and its value can be measured reliably. These criteria will normally be met following probate once the executor(s) of the estate has established that there are sufficient assets in the estate, after settling liabilities, to pay the legacy.

PBE34B.6 Evidence that the executor(s) has determined that a payment can be made, may arise on the agreement of the estate’s accounts or notification that payment will be made. Where notification is received after the year-end but it is clear that the executor(s) has agreed prior to the year-end that the legacy can be paid, the legacy is accrued in the financial statements. The certainty and measurability of the receipt may be affected by subsequent events such as valuations and disputes.

PBE34B.7 Entities that are in receipt of numerous immaterial legacies for which individual identification would be burdensome may take a portfolio approach.

Services

PBE34B.8 Donated services that can be reasonably quantified shall be recognised in the financial statements when they are received.

PBE34B.9 Donated services that are consumed immediately are usually recognised as an expense. However, there may be circumstances when a service is used in the production of an asset, for example erecting a building. In these cases, the associated donated service (eg plumbing and electrical services) would be recognised as a part of the cost of that asset.

PBE34B.10 Donated services that can be reasonably quantified include donated facilities, such as office accommodation, services that would otherwise have been purchased and services usually provided by an individual or an entity as part of their trade or profession for a fee.

PBE34B.11 It is expected that contributions made by volunteers cannot be reasonably quantified and therefore these services shall not be recognised.

PBE34B.12 Paragraph PBE34.74(c) requires an entity to disclose other forms of resources from non-exchange transactions from which the entity has benefited. This will include the disclosure of unrecognised volunteer services.

Performance-related conditions

PBE34B.13 Some resources are given with performance-related conditions attached which require the recipient to use the resources to provide a specified level of service in order to be entitled to retain the resources. An entity will not recognise income from those resources until these performance-related conditions have been met.

PBE34B.14 However, some requirements are stated so broadly that they do not actually impose a performance-related condition on the recipient. In these cases the recipient will recognise income on receipt of the transfer of resources.

Measurement

PBE34B.15 Paragraph PBE34.73(a) requires donated services and facilities to be measured at the value to the entity. This requirement only applies to those services and facilities that would otherwise have been purchased by the entity. The value placed on these services and facilities should be the estimated value to the entity of the service or facility received, this will be the price the entity estimates it would pay in the open market for a service or facility of equivalent utility to the entity.

PBE34B.16 Paragraph PBE34.73(b) requires resources received or receivable, that are not services or facilities, to be measured at their fair value. These fair values are usually the price that the entity would have to pay on the open market for an equivalent resource.

PBE34B.17 When there is no direct evidence of an open market value for an equivalent item a value may be derived from sources such as:

(a) the cost of the item to the donor; or

(b) in the case of goods that are expected to be sold, the estimated resale value (which may reflect the amount actually realised) after deducting the cost to sell the goods.

PBE34B.18 Donated services are recognised as income and an equivalent amount shall be recognised as an expense in income and expenditure, unless the expense can be capitalised as part of the cost of an asset.

Public Benefit Entity Combinations

Extract from FRS102: Section PBE 34.75-. PBE 34.86

PBE34.75 Paragraphs PBE34.76 to PBE34.86 apply only to public benefit entities for the following categories of entity combinations which involve a whole entity or parts of an entity combining with another entity:

(a) combinations at nil or nominal consideration which are in substance a gift; and

(b) combinations which meet the definition and criteria of a merger.

PBE34.76 Combinations which are determined to be acquisitions shall be accounted for in accordance with Section 19 Business Combinations and Goodwill.

Combinations that are in substance a gift

Accounting treatment and disclosure

PBE34.77 A combination that is in substance a gift shall be accounted for in accordance with Section 19 except for the matters addressed in paragraphs PBE34.78 and PBE34.79 below.

PBE34.78 Any excess of the fair value of the assets received over the fair value of the liabilities assumed is recognised as a gain in income and expenditure. This gain represents the gift of the value of one entity to another and shall be recognised as income.

PBE34.79 Any excess of the fair value of the liabilities assumed over the fair value of the assets received is recognised as a loss in income and expenditure. This loss represents the net obligations assumed, for which the receiving entity has not received a financial reward and shall be recognised as an expense.

Combinations that are a merger

PBE34.80 Unless it is not permitted by the statutory framework under which a public benefit entity report, an entity combination that is a merger shall apply merger accounting as prescribed below. If merger accounting is not permitted, an entity combination shall be accounted for as an acquisition in accordance with Section 19.

PBE34.81 Any entity combination:

(a) which is neither a combination that is in substance a gift nor a merger; or

(b) for which merger accounting is not permitted by the statutory framework under which the public benefit entity reports shall be accounted for as an acquisition in accordance with Section 19.

Accounting treatment

PBE34.82 Under merger accounting the carrying value of the assets and liabilities of the parties to the combination are not adjusted to fair value, although adjustments shall be made to achieve uniformity of accounting policies across the combining entities.

PBE34.83 The results and cash flows of all the combining entities shall be brought into the financial statements of the newly formed entity from the beginning of the financial period in which the merger occurs.

PBE34.84 The comparative amounts shall be restated by including the results for all the combining entities for the previous accounting period and their statement of financial positions for the previous reporting date. The comparative figures shall be marked as ‘combined’ figures.

PBE34.85 All costs associated with the merger shall be charged as an expense in the period incurred.

Disclosure

PBE34.86 For each entity combination accounted for as a merger in the reporting period the following shall be disclosed in the newly formed entity’s financial statements:

(a) the names and descriptions of the combining entities or businesses;

(b) the date of the merger;

(c) an analysis of the principal components of the current year’s total comprehensive income to indicate:

(i) the amounts relating to the newly formed merged entity for the period after the date of the merger; and

(ii) the amounts relating to each party to the merger up to the date of the merger.

(d) an analysis of the previous year’s total comprehensive income between each party to the merger;

(e) the aggregate carrying value of the net assets of each party to the merger at the date of the merger; and

(f) the nature and amount of any significant adjustments required to align accounting policies and an explanation of any further adjustments made to net assets as a result of the merger.

Public Benefit Entity Concessionary Loans

Extract from FRS102: Section PBE 34.87-. PBE 34.97

PBE34.87 Paragraphs PBE34.89 to PBE34.97 address the recognition, measurement and disclosure of public benefit entity concessionary loan arrangements within the financial statements of public benefit entities or entities within a public benefit entity group making or receiving public benefit entity concessionary loans. These paragraphs apply to public benefit entity concessionary loan arrangements only and are not applicable to loans which are at a market rate or to other commercial arrangements.

PBE34.88 Public benefit entity concessionary loans are loans made or received between a public benefit entity or an entity within the public benefit entity group, and another party at below the prevailing market rate of interest that are not repayable on demand and are for the purposes of furthering the objectives of the public benefit entity or public benefit entity parent.

Accounting treatment

PBE34.89 Entities making or receiving public benefit entity concessionary loans shall use either:

(a) the recognition, measurement and disclosure requirements in Section 11 Basic Financial Instruments or Section 12 Other Financial Instruments Issues (for example, Section 11 requires initial measurement at fair value and subsequent measurement at amortised cost using the effective interest method); or

(b) the accounting treatment set out in paragraphs PBE34.90 to PBE34.97 below.

A public benefit entity or an entity within a public benefit entity group shall apply the same accounting policy to concessionary loans both made and received.

Initial measurement

PBE34.90 A public benefit entity or an entity within a public benefit entity group making or receiving concessionary loans shall initially measure these arrangements at the amount received or paid and recognise them in the statement of financial position.

Subsequent measurement

PBE34.91 In subsequent years, the carrying amount of concessionary loans in the financial statements shall be adjusted to reflect any accrued interest payable or receivable.

PBE34.92 To the extent that a loan that has been made is irrecoverable, an impairment loss shall be recognised in income and expenditure.

Presentation and disclosure

PBE34.93 The entity shall present concessionary loans made and concessionary loans received either as a separate line items on the face of the statement of financial position or in the notes to the financial statements.

PBE34.94 Concessionary loans shall be presented separately between amounts repayable or receivable within one year and amounts repayable or receivable after more than one year.

PBE34.95 The entity shall disclose in the summary of significant accounting policies the measurement basis used for concessionary loans and any other accounting policies which are relevant to the understanding of these transactions within the financial statements.

PBE34.96 The entity shall disclose the following:

(a) the terms and conditions of concessionary loan arrangements, for example the interest rate, any security provided and the terms of the repayment; and

(b) the value of concessionary loans which have been committed but not taken up at the year end.

PBE34.97 Concessionary loans made or received shall be disclosed separately. However multiple loans made or received may be disclosed in aggregate, providing that such aggregation does not obscure significant information.

34.15.2 OmniPro comment

34.15.2.1 Public benefit entity defined

A public benefit entity is defined as one ‘whose primary objective is to provide goods or services for the general public, community or social benefit and where any equity is provided with a view to supporting the entity’s primary objectives rather than with a view to providing a financial return to equity providers, shareholders or members’.

The following entities normally fall within this definition:

- Charities

- Registered social landlords

- Further education colleges

- High education institutions

- Clubs, societies, trade unions etc.

The key point in order for it to be classed as a public benefit entity is that the entities primary purpose should not be to provide economic benefits to its investors (i.e. cannot provide returns proportionally to its members in any way). An entity should consider its primary purposes in determining whether it is a PBE.

A public benefit entity group is defined in Appendix I of FRS 102 as ‘a public benefit entity parent and all of its wholly owned subsidiaries. The key thing is that they must wholly owned subsidiaries in order to be classed as a PBE group.’

34.15.2.1.1 Requirement to disclose that an entity is a public benefit entity

Where a PBE applies one or more of the PBE elements in section 34 it must disclose this in the form of an unreserved statement in the financial statements as required by Section 3.3A of FRS 102.

34.15.2.2 Special rules for public benefit entities

The special provisions for PBE’s are:

34.15.2.2.1 Assets held for provision of social benefits

Asset held for provision of social benefits is not required to be classified as an investment property and instead remains as property, plant and equipment and accounted for in line with Section 17. Obviously if a PBE specifically holds such an asset for capital appreciation then it must be accounted for in accordance with Section 16.

34.15.2.2.2 Income resources from non-exchange transactions.

34.15.2.2.2.1 Overview

Sections PBE34.64 to 34.74 of FRS 102 provide the guidance on non-exchange transactions. Appendix B of Section 34 also provides guidance. Examples include cash, property received from donators or received in a will.

34.15.2.2.2.2 Accounting for non-exchange accounting

34.15.2.2.2.2.1 Recognition for goods and measurement for goods

The accounting for such transactions as stated in Section PBE34.67 of FRS 102 is:

- If the transaction does not impose performance related conditions on recipient = recognise in income when resources are received or receivable and can reliably measured. If the resource cannot be measured reliably then it cannot be recognised until it is sold. It is recognised in line with normal recognition criteria.

- If transaction does impose performance related conditions on recipient= recognise in income when the performance related conditions are met

- Incoming resources are received in advance and before revenue recognition criteria are satisfied = recognise a liability i.e. deferred income.

Section PBE34.73(B) of FRS 102 requires all donations other than services and the provision of facilities to be measured at the fair value of the resources received or receivable

34.15.2.2.2.2.1.1 Performance related conditions defined

A performance related condition is defined in Appendix I of FRS 102 as ‘a condition that requires the performance of a particular level of service or units of output to be delivered, with payment of, or entitlement to, the resources conditional on that performance’.

34.15.2.2.2.2.1.2 Conditions that are not performance related

Conditions attached to a donation which are not defined as performance related conditions do not prevent the revenue being recognised as stated in Section PBE34.68 of FRS 102 e.g. a condition that the money be invested in property but if the property is sold then it is repayable. In this case the revenue can be recognised and a liability only recognised if it is probable the property would be sold.

34.15.2.2.2.2.1.3 Examples of non-exchange resource transactions received in the form of goods.

Examples of non-exchange transactions goods (incorporating Appendix B of Section 34 of FRS 102 guidance)

1. Specific rule – Cash Donations

- Recognised on a receivable basis assuming general conditions are met

2. Specific rule – Legacies – recognise when

- There is grant of probate; and

- The executors have established that there is sufficient assets in the estate, after settling liabilities; and

- Any conditions attached to the legacy are either within the control of the charity or have been met

Example 8: Legacies (Section 34 of FRS 102 & Section 5 of SORP)

Charity A has been informed by a solicitor that it has been identified as a beneficiary of a persons will. The solicitor has stated that as of yet the amount of the legacy is not certain as it has not gone through probate, expenses have still to be paid and the interest is in the residue of the estate. The solicitor has stated a figure of CU100k – CU150k however this is only indicative.

Can the charity recognise any income in the current year?

The rules for recognition of legacies are (PBE34B.5 to 7 of FRS 102):

- There is grant of probate; and

- The executors have established that there is sufficient assets in the estate, after settling liabilities; and

- Any conditions attached to the legacy are either within the control of the charity or have been met

On this basis, the charity cannot recognise income in the current year as although there is entitlement to the funds and although it is probable economic benefits will flow, the amount of the legacy cannot be measured reliably hence it should not be recognised at that time. In addition there is no grant of probate.

However a contingent asset would need to be included in the notes detailing the legacy.

Example 9: Legacies (Section 34 of FRS 102 & Section 5 of SORP)

If we take example 1 and this time assume that the executor has determined that a payment will be made to the charity following the agreement of the estate’s accounts and that a reliable estimate of CU100k can be given.

Can the charity recognise any income in the current year?

Yes as long as the likelihood of receipt is probable (as reliable estimate and entitlement has been established) the legacy would be recognised as income in the SOFA/I&E/P&L in the current year. The journals would be as follows assuming it will be receivable within 12 months of year end:

| CU | CU | |

| Dr legacy debtor | 100,000 | |

| Cr donations and legacy income in SOFA/income/turnover in I&E | 100,000 |

If we assume that the executor believes it will not be received until 24 months after the recognition of income, there would be a requirement to present value the CU100,000 at a discount rate equal to the rate the charity could get on a deposit account for a similar length. Assume the PV is CU85,000 and CU9,000 and CU6,000 of this unwinds in the first and second year after recognition. The journals would be to:

| CU | CU | |

| Dr legacy debtor | 85,000 | |

| Cr donations and legacy income in SOFA or turnover in I&E | 85,000 |

Being journal to recognise income at present value.

Then the below journal should be posted to reflect the unwinding of the discount:

| CU | CU | |

| Dr legacy debtor | 9,000 | |

| Cr donations and legacy income in SOFA OR interest income in P&L/I&E | 9,000 |

Example 10: Legacies (Section 34 of FRS 102 & Section 5 of SORP)

If we take example 9 and 6 months later it transpires that only CU60,000 will be received.

What are the journals required (ignoring present valuing):

The journals required are to:

| CU | CU | |

| Dr donations and legacy income in SOFA/ Income or turnover in I&E/P&L | 40,000 | |

| Cr legacy debtor | 40,000 |

Example 11: Legacies (Section 34 of FRS 102 & Section 5 of SORP)

Charity A has been notified by an executor that a payment will be made.

Can this be recognised in income?

Yes this should be recognised at that time.

Example 12: Legacies (Section 34 of FRS 102 & Section 5 of SORP)

If we take example 11 and assume the notification was received post year end but before the accounts are authorised for issue. In this case can the charity recognise this legacy in income for the current year even though notification was not received until after year end?

Answer: It depends – If it is clear that the payment had been agreed by the executor prior to the end of the reporting period, it should be recognised as income and included as a receivable.

Example 13: Legacies (Section 34 of FRS 102 & Section 5 of SORP)

Charity A has been informed by an executor that it is entitled to a house on the death of a life tenant.

Can the charity recognise the market value of the house at that time?

Answer: No. It can only recognise it in income once the life tenant dies. However it should be disclosed as a contingent asset.

3) Donated goods and services (Section 34 of FRS 102 & S.6 of SORP)

Donated goods and services – recognise when:

- Entitlement

- It is probable future economic activities will flow

- It can be reliably estimated

Income should be recognised on the above basis unless it is impractical to value the goods/services given the low value or the costs outweigh the benefits to the readers in which case it should be measured when sold

If recognised initially on receipt, then recognise credit in income and a corresponding debit in expenses/stock/fixed assets as applicable

If fair value cannot be determined easily then determine the value by:

- Assessing cost to the donor; or

- The expected resale value after deducting costs to sell

If fair value recognised in stock initially, then on the future same:

- Post the debit for the recognition of stock to income & set against sale amount

If fair value donated services – recognise at the fair value to charity (what would charity have to pay if they got someone else)

Donated time of volunteers is not required to be recognised

- In assessing whether a person is volunteer or a person providing services & hence income to be recognised determine if:

- The person perform a business of the service that they provide to the charity; or

- The person is only ancillary to other charity staff

Example 14: Donated goods or services – fixed assets

Charity A received a gift in the form of a property which will be used for the purposes of its trade.

In this case under Section 6.6 of SORP or Section PBE34.67 to 34.70 & PBE34B.1 of FRS 102 income should be recognised when the charity:

- Has entitlement; and

- Can reliably measure the asset/gift; and

- It is probable economic benefits will flow to the charity.

It should initially be measured at fair value unless it is impractical to measure. Assume the fair value of this asset was CU500,000

The journals required once the recognition criteria are met are as detailed below:

| CU | CU | |

| Dr Tangible fixed assets | 500,000 | |

| Cr donations and legacies in the SOFA OR Turnover/income in I&E or P&L | 500,000 | |

From then on, the asset is depreciated over its useful economic life as would be the case for any other fixed asset. Note if a restriction was imposed as part of the gift that it cannot be disposed the fair value should be adjusted downwards to reflect this restriction.

If this was a property which had sitting tenants and the charity decided to continue to lease it out then this would be classified as an investment property and included within investments in the financial statements for SORP accounts or within tangible fixed assets under FRS 102 and would have to carried at fair value. There would be no depreciation instead the movement would be recognised in the line ‘gain/loss on investments’ in the SOFA for SORP Accounts or in the P&L/I&E possibly within other operating income if just FRS 102 accounts are prepared.

Example 15: Donated goods or services – donated goods held for resale – impractical to measure

Charity A operates a charity shop as one of the activities of the charity and receives donated goods which it then sells on.

In this case under Section 6.6 of SORP or Section PBE34.67 to 70 & PBE34B.1 to 2 of FRS 102, income should be recognised when the charity:

- Has entitlement; and

- Can reliably measure the asset/gift; and

- It is probable economic benefits will flow to the charity.

It should initially be measured at fair value unless it is impractical to measure or would result in undue cost given the value of the donated goods. If this is the case the donated goods should be recognised when sold. If fair value cannot be determined then the value placed on it should be obtained by:

- Assessing the cost of the item to the donor

- Or goods which are expected to be sold, the estimate resale value after deducting costs to sell

If we assume that it is impractical to measure given the low value of the goods, then on initial receipt, income should not be recognised instead under S6.10 of SORP or PBE34.70 of FRS 102, the income is recognised when sold. Assume for this example this item was sold for CU50. The journals required on sale would be to:

| CU | CU | |

| Dr Bank | 50 | |

| Cr income from other trading activities in the SOFA* / Turnover/income in P&L/I&E | 50 |

* Note if the shop is the primary purpose of the charity then the Credit would go to ‘income from charitable activities’.

Note if we assume that these were goods which were used by the Charity itself as opposed to being sold on, the following journals would be required:

| CU | CU | |

| Dr expenditure on charitable activities in the SOFA OR Administrative expenses in P&L/I&E | 50 | |

| Cr income from other trading activities in the SOFA* OR Turnover/income in P&L/I&E | 50 |

* Note if the shop is the primary purpose of the charity then the Credit would go to ‘income from charitable activities’.

Example 16: Donated goods or services – donated goods held for resale – practical to measure

If we take example 15 and this time assume that the goods can be measured. Assume the fair value of the donated good was CU1,000 and the cost of onward sale is CU50.

Given that it can be measured assuming the recognition rules (e.g. on receipt) have been met the journal would be to:

| CU | CU | |

| Dr stock on the balance sheet | 950 | |

| Cr income – donations in the SOFA OR Turnover/income in P&L/I&E | 950 |

Note as this is recognised in stock it should be reviewed for impairment and impairment booked if required (required by Section 10 & Section 12 of SORP OR S.27 of FRS 102).

| For FRS 102 SORP | CU | CU |

| Dr income from other trading activities in the SOFA* OR Turnover/income in P&L/I&E | 950 | |

| Dr bank/debtors | 1,000 | |

| Cr stock on balance sheet | 950 | |

| Cr income from other trading activities in the SOFA OR Turnover/income in P&L/I&E | 1,000 |

* Note if the shop is the primary purpose of the charity then the Credit would go to ‘income from charitable activities’.

| FRS 102 – Non SORP assuming no element of SORP adopted | CU | CU |

| Dr cost of sales/administrative expenses | 950 | |

| Cr stock on the balance sheet | 950 | |

| Dr Bank | 1,000 | |

| Cr Turnover/income in P&L/I&E | 1,000 |

Example 17: Donated goods or services – donated goods held for resale – Other trading activities not main charitable activity

Charity A’s primary purpose is to provide knowledge and support to persons effected by a certain physical condition. It also carried on shops where donated goods are provided. The income from the shops in the year was CU1,000 and the expenses were CU 800 which includes wage costs.

The journals required under FRS 102 (non-SORP) are:

| CU | CU | |

| Dr Bank | 1,000 | |

| Cr Turnover/income | 1,000 | |

| Dr administrative expenses | 800 | |

| Cr Bank | 800 |

The journals required under FRS 102 SORP are:

| CU | CU | |

| Dr income from other trading activities in the SOFA | 800 | |

| Dr bank/debtors | 200 | |

| Cr income from other trading activities in the SOFA | 1,000 |

34.15.2.2.2.2.2 Non-exchange resources received in the form of services/facilities

34.15.2.2.2.2.2.1 Overview

Section PBE 34.72 of FRS 102 provides the guidance for accounting non-exchange resources received in the form of services or use of facilities.

Examples would include;

- Donated facilities e.g. office space

- Services that would have to be purchased had it not been got for free

- Services provided usually as part of a trade or profession but provided free of charge.

34.15.2.2.2.2.2.2 Recognition and measurement

In this instance the PBE should recognise revenue for the value of the service etc provided and recognise an expense at the very same time in the profit and loss or alternatively if it is work done on a fixed asset/inventory it would be included as an asset within the relevant asset class (Section PBE 34.72 of FRS 102) . Where it cannot be measured, it should be recognised at the cost of the item to the donor or the estimated sales value when sold on.(Section PBE34B.17 of FRS 102 refers)

34.15.2.2.2.2.2.2.1 Examples of non-exchange Transactions where services/facilities provided

Example 18: Donated goods or services – donated services

The rules with regard to recognition of income where services are provided are similar to where donated goods are received as detailed in the examples above. However where services or facilities are given for the charity’s own use they should be measured initially at the value to the charity (i.e. the amount the charity would have to be pay if it were to -pay for this facility service in the open market). Income should be recognised when the service or facility is received.

Charity A received the services of an electrician to repair wiring in the charity’s premises at no charge. If the charity were to get an electrician it would cost the charity CU2,000. Therefore the journals required are:

| CU | CU | |

| Dr expenditure on charitable activities in the SOFA OR administrative expense in P&L/I&E | 2,000 | |

| Cr donations in the SOFA OR Income/Turnover in P&L/I&E | 2,000 |

If this work related to the construction of its premises it may be possible to capitalise this cost and then depreciate.

If this time we assume the charity obtains an office rent free. Then the journal would be to:

| CU | CU | |

| Dr expenditure on charitable activities in the SOFA OR administrative expense in P&L/I&E | 2,000 | |

| Cr donations in the SOFA OR Income/Turnover in P&L/I&E | 2,000 |

Here S.6.31 of SORP or PBE34.74 of FRS 102 requires disclosure of amounts and nature of non-exchange transactions recognised in the accounts.

Note the donated time of volunteers is not required to be recognised in the financial statements (usually individuals who do not perform a business on their own account in the service they provide).

34.15.2.2.3 Public benefit entity combinations

34.15.2.2.3.1 Overview

Sections PBE 34.75 to PBE 34.84 of FRS 102 provide the guidance for accounting for business combinations.

34.15.2.2.3.1.1 Business combinations defined

Appendix I of FRS 102 defines a business combination as the ‘bringing together of separate entities or businesses into one reporting entity’.

34.15.2.2.3.2 Accounting Requirements

The accounting requirements for a PBE depends on the type of business combination:If the business combination:

34.15.2.2.3.2.1 Gift of a business for nil or nominal consideration

- Is in substance a gift of a business for nil or nominal consideration= recognise the assets/liabilities at fair value with a corresponding gain/loss shown in the profit and loss (i.e. the PBE must follow section 19 with regard to fair valuing assets and liabilities see 19.8.1.2.2). See Section PBE 34.77 to PBE 34.79 of FRS 102.

An example of this would be a charity giving a business to another charity.

34.15.2.2.3.2.1.1 Example of business combinations which is a gift that is not a merger

Example 19: Business Combinations: Gifts of business etc.:

Charity A was gifted a business during the year (which was not incorporated). The excess of fair value over liabilities at the date of the gift was €100,000 (split €150k assets/€50k liabilities).

If there is a transfer which is in substance a gift then this should be recognised as income (within other income in the SOFA) if the fair value of assets exceed the fair value of liabilities at time of gift. This is stated in Section 24.33 of SORP and Section 34 PBE34.77-79 of FRS 102.

If liabilities exceed asset fair value – recognised as an expense in SOFA or P&L/I&E.

Journals required

| CU | CU | |

| Dr Assets etc. | 150,000 | |

| Cr Liabilities etc. | 50,000 | |

| Cr– Other income in SOFA or turnover in P&L/ I&E | 100,000 | |

| Being journal to reflect the gain on gift of business | ||

If in the above example, these were shares the journals would be to

| CU | CU | |

| Dr Investment in shares on Balance sheet | 100,000 | |

| Cr– Other income in SOFA turnover in P&L/ I&E | 100,000 | |

| Being journal to reflect the gain on gift of shares in business in the entity accounts | ||

In the consolidated financial statements, the €100,000 would be recognised as goodwill on the balance sheet and amortised.

Rules as per section 19 of FRS 102. See examples at 19.13.2.2.

34.15.2.2.3.2.1.2 Disclosures

As made clear in Section PBE34.77 of FRS 102, the disclosure requirements detailed in Section 19 at 19.14 must be met.

34.15.2.2.3.2.2 Merger

2) Meets the definition and criteria of a merger = merger accounting can be applied (Sections PBE 34.80 to PBE 34.85 of FRS 102). This is discussed further in Section 19 and Section 9 of this manual at 19.13.2.2.

In order to meet the definition of a merger as given in Appendix 1 of FRS 102, all of the following criteria must be met:

– no party is portrayed as either the acquiree or acquirer either by its board or any other party;

– there is no significant change in the class of beneficiaries of the combining entities or the purpose of the benefits provided as a result of the combinations

All parties to the combination, as represented by the board, participate in establishing the management structure of the combined entity and in selecting the management personnel, and such decisions are made on the basis of consensus between the parties to the combination rather than purely by exercise of voting rights (Appendix I of FRS 102). Where the PBE rules do not permit merger accounting, acquisition accounting should be used (see 34.14.2.2.3.2.3).

Where merger accounting is applied, the fair values of the assets and liabilities are not adjusted and remain at the book values other than changes required for uniform accounting policies as stated in Section PBE 34.82 to PBE 34.85 of FRS 102. Merger accounting is discussed in further detail in Section 19 of the manual at 19.13.2.2.

34.15.2.2.3.2.2.1 Disclosure

The disclosure requirements where merger accounting is applied is detailed in Section PBE34.86 of FRS 102.

34.15.2.2.3.2.2 Examples illustrating merger accounting

Business Combinations: (S.27 of SORP & Section 34 of FRS 102)

Example 20: Business Combinations: Mergers

Charity A and Charity B have a year end of 31 December 2016 and are CLG’s. Charity B merged with charity A on 1 January 2017. Under Section 34 of FRS 102 and S of SORP this is required to be accounted for under merger accounting. At the date of the merger the net funds of Charity B was CU100,000 split CU65,000 unrestricted and CU35,000 restricted (made up CU150,000 assets and CU50,000 liabilities). At the start of the comparative period (i.e. 1 January 2016) the net funds of Charity B was CU90,000 split CU60,000 unrestricted and CU30,000 restricted (made up CU140,000 assets and CU50,000 liabilities). The income in 31/12/16 for charity B was income of CU160k and costs of CU150k (profit split 5k to restricted & 5k to unrestricted).

The cost of the merger was CU50,000.

Section 34 PBE34.80-81 of FRS 102 and Section 27 of SORP lays out the accounting treatment for mergers.

It is a Merger only if all of the below apply:

- No party portrayed as acquirer or acquire;

- No significant change in class of beneficiaries of the combined entities;

- All parties are represented on the board and decisions made to conscious.

Merger accounting requires the following in the 31 December 2017 accounts:

- Charity A to recognise the net funds of charity B at 31 December 2014 in a merger reserve (there is no fair value rules – it is transferred in at the carrying amount stated in Charity B at time of transfer)

- Comparative amounts of Charity A as previously stated to be adjusted to include Charity B results in balance sheet and SOFA/profit and loss account

- Current year amounts Charity A to be adjusted to include Charity B results in balance sheet and SOFA/ profit and loss account for the full year (regardless of when it was acquired in that year).

- Cost associated with the merger must be expensed in the 31 December 2017 year in Charity A accounts.

- If restricted funds in Charity B, then should be shown as restricted in combined charity if SORP accounts prepared.

Impact on 31 December 2016 accounts for Charity B

- Consideration should be given to the audit report implications where accounts are required for Charity B by the Charities Regulator or Grant provider:

- Not companies Act requirement as Co. is considered dissolved– maybe carry out agreed upon procedures – agree who signs the accounts

- Implications on audit report – present on Break up basis??

- Post balance sheet event note

Impact on 31 December 2016 accounts for Charity A

- Post balance sheet event note;

Impact on 31 December 2017 accounts for Charity A

The following journals are required to be posted to the opening balance sheet within the comparative year (31/12/16)

| CU | CU | |

| Dr Fixed assets, debtors, etc. etc. | 140,000 | |

| Cr– Merger Reserve – unrestricted fund under heading ‘funds of the charity’ in Balance Sheet or In capital and reserves for non SORP | 60,000 | |

| Cr– Merger Reserve – restricted fund under heading ‘funds of the charity’ in Balance Sheet | 30,000 | |

| Cr Creditors etc. etc. | 50,000 | |

| Being journal to reflect the merger and get correct net assets at start of comparative period. | ||

The following journals are required to be posted to the comparative year in Charity B books (31/12/16)

| CU | CU | |

| Dr Fixed assets, debtors, etc. etc. | 10,000 | |

| Dr Expenditure in SOFA/P&L in relevant area in unrestricted fund column in SOFA/I&E which follow through to Merger Reserve – unrestricted fund under heading ‘funds of the charity’ in Balance Sheet (65k-60k) | 75,000 | |

| Dr Expenditure in SOFA/P&L in relevant area in restricted fund column in SOFA/I&E if SORP accounts prepared. which follow through to Merger Reserve – restricted fund under heading ‘funds of the charity’ in Balance Sheet (34k-30k) | 75,000 | |

| Cr– Income in relevant heading in unrestricted fund column in SOFA/I&E which follow through to Merger Reserve – unrestricted fund under heading ‘funds of the charity’ in Balance Sheet (65k-60k) | 80,000 | |

| Cr– Income in relevant heading in restricted fund column in SOFA/I&E which follow through to Merger Reserve – restricted fund under heading ‘funds of the charity’ in Balance Sheet (34k-30k) | 80,000 | |

| Cr Creditors etc. etc. | – | |

| Being journal to reflect the merger and get correct net assets at end of comparative period & show results in the comparative year inclusive of Charity B. | ||

The journals required in 2017 – None assuming the trial balance incorporates the results of the combined entity from 1 January. The CU50,000 expenses should be expensed into SOFA/P&L possibly as exceptional items if material.

34.15.2.2.3.2.3 Meets the definition of a true acquisition and the purchase method applies

- Meets the definition of an acquisition = acquisition accounting at fair value is required (See PBE 34.81 of FRS 102). Acquisition accounting applies the rules set out in Section 19 of FRS 102 i.e. measure the fair value of all assets and liabilities received and allocates the consideration between them. See details of acquisition accounting/purchase method at 19.5.2, 19.6.2, 19.7.2, 19.8.1.2 and 19.10.2

34.15.2.2.3.2.3.1 Example business combination: Not a merger or gift – Purchase accounting method

See examples at 19.5.2, 19.6.2, 19.7.2, 19.8.1.2 and 19.10.2

34.15.2.2.4 Public benefit concessionary loans

34.15.2.2.4.1 Overview

Sections PBE 34.87 to PBE 34.97 of FRS 102 provide the accounting treatment and disclosure requirements for public benefit entity concessionary loans

34.15.2.2.4.2 Public benefit entity loan defined

Appendix I of FRS 102 defines a public benefit entity loan as ‘a loan made or received between a public benefit entity or an entity within a public benefit entity group and another party:

- At below prevailing market rates of interest; and

- That is not repayable on demand; and

- Is for the purposes of furthering the objectives of the public benefit entity parent (Section PBE 34.88 of FRS 102 refers).

34.15.2.2.4.3 Accounting treatment of public benefit concessionary loans choices

Where all three of the requirements in 34.14.2.2.4.2 are met, the PBE does not have to account for these loans under Section 11 or Section 12 of FRS 102 (i.e. measure these at the present value of the future cash flows using a market interest rate). Instead the entity is provided with an accounting policy choice to apply either, (as stated in Section PBE 34.89 of FRS 102):

- The recognition, measurement and disclosure requirements of Section 11 of FRS 102 (i.e. at amortised cost) If this option is chosen they must apply all the disclosure requirements of Section 11 and Section 12 of FRS 102; or

- Recognise the loan received or paid at the actual amount received or paid with no discounting required and subsequently adjusted for any interest charged (if any) and repayments made (Section PBE 34.90 to 34.92 of FRS 102).

The above policy choice should be applied consistently, it must treat loans received or given in the same way.

34.15.2.2.4.4 Disclosures

Section PBE34.97 of FRS 102 details the disclosure requirements for public benefit concessionary loans. See details 34.14.2.2.4.5.

Extract from the accounting policies note

Public benefit concessionary loans – programme related assets [If Required]

Public benefit concessionary loans are initially measured at the amount received or paid in the balance sheet and subsequently adjusted to reflect any accrued interest payable or receivable and repayments made/received. Public benefit entity concessionary loans are loans made or received between a public benefit entity and another party at below the prevailing market rate of interest that are not repayable on demand and are for the purposes of furthering the objectives of the public benefit entity. To the extent that a loan that has been made is irrevocable, an impairment loss shall be recognised in the statement of financial activities within the expenditure on charitable activities cost.

Extract from the notes to the financial statements with regard to concessionary loans:

1. DEBTORS

| 2015 | 2014 | |

| CU’000 | CU’000 | |

| Trade debtors | 100 | 500 |

| Amounts due on public benefit entity concessionary loans | – | – |

| Amount receivable from non-exchange transactions | – | – |

| Legacies | 50 | – |

| Other debtors | – | – |

| Accrued income | – | – |

| Prepayments | 650 | 800 |

| 800 | 1,300 |

The fair values of trade and other receivables approximate to their carrying amounts. Trade debtors are stated after provisions for impairments of CUXXX (2014: CUXXX).

The public benefit entity concessionary loan is interest free and repayable on demand.

2. CREDITORS: AMOUNTS FALLING DUE WITHIN ONE YEAR

| 2015 | 2014 | |

| CU’000 | CU’000 | |

| Bank loans and overdrafts | – | – |

| Trade creditors | 500 | 400 |

| Amounts payable on public benefit entity concessionary loans (see note X) | – | – |

| Deferred income (see note X) | – | – |

| Accruals | 200 | 100 |

| Payments received on account for contracts | – | – |

| Payments received on account for performance related grants | – | – |

| Other creditors | – | – |

| Accruals for grants payable | – | – |

| PAYE/PRSI | 54 | 77 |

| 754 | 577 |

3. DETAILS OF BORROWINGS (IF ANY)

| Within 1 year | Between 1 & 2 years | Between 2 & 5 years | After 5 years | Total | |

| CU’000 | CU’000 | CU’000 | CU’000 | CU’000 | |

| Repayable other than by instalments | |||||

| Bank Overdrafts | – | – | – | – | – |

| Public benefit entity concessionary loans | – | – | – | – | – |

| Finance Leases | – | – | – | – | – |

| Repayable by instalments | – | – | – | – | – |

| Term Loan |

The bank facilities are secured by a debenture incorporating fixed and floating charges over the assets of the company and personal guarantees from the Directors.

The facilities expiring within one year are annual facilities subject to review at various dates during 2015/2016. Interest is payable at a fixed rate of x% OR at the standard variable rate of interest of X%.

The public benefit entity concessionary loan is interest free and repayable on 31 December 2019.

34.15.2.2.4.5 Examples of concessionary loans

Example 21: Concessionary loans – option not to discount

Charity A received a loan from a third party/subsidiary company for CU100,000 which is interest free or below market interest rates and not repayable on demand (repayable in 5 years time). This loan was provided to further the charitable activities (e.g. to purchase a building to be used to provide charitable services).

In this instance the entity has a choice to carry this loan at amortised cost (discounting at a market rate of interest on initial recognition as a finance arrangement exists) under the rules of Section 11 of FRS 102 and the Charities SORP (assuming it meets the requirement of a basic financial instrument) or apply Section 21 of Charities SORP or Section 34 of FRS 102 to carrying this loan on initial recognition at the transaction amount i.e. the amount of the loan received less transaction costs – no discounting required.

In order to classify as a concessionary loan it must have been received/given in order to advance the charitable objectives of the charity.

If this was a loan given to a beneficiary at favourable rates it would be classified as a programme related investment/social investment.

Based on the above facts this loan meets the definition of a concessionary loan so the initial recognition journals are:

| CU | CU | |

| Dr bank | 100,000 | |

| Cr loan | 100,000 |

Being journal to reflect the receipt on initial recognition. No discounting is required.

The above loan is defined as programme related loans under SORP and should be disclosed as such.

Note where a concessionary loan exists, the accounting policy must be disclosed as well as it being highlighted as a concessionary loan and the terms of same should be disclosed.

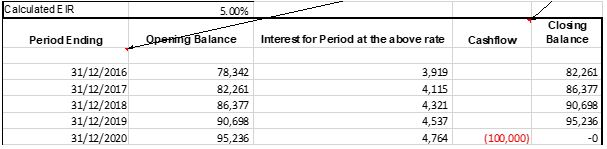

Example 22: Concessionary loans – option to discount

If we take example 21 above and this time assume the alternative treatment was applied then the difference between the discounted amount and the amount received would be shown as income initially and unwinding would be posted to the line ‘cost of charitable activities in the SOFA as an interest cost over the life of the loan in line with the effective interest method.

NOTE WHERE OPTION ONE IS CHOSEN S.21.26 OF SORP REQUIRES THAT WHERE THE AMOUNT IS REPAYABLE WITHIN ONE YEAR OR IS REPAYABLE ON DEMAND IT DOES NOT NEED TO BE DISCOUNTED (I.E. THE RULES IN NUMBER 2 APPLY).

| CU | CU | |

| Dr bank | 100,000 | |

| Cr loan | 78,342 | |

| Cr Income from donations and legacies in the SOFA OR Turnover/ income in P&L/I&E | 21,658 |

Being journal to reflect the receipt on initial recognition

| CU | CU | |

| Dr cost of charitable activities – Interest expense in the SOFA OR Interest expense in P&L/I&E | 3,919 | |

| Cr loan | 3,919 |

Being journal to recognise the unwinding of the interest in the first year

34.15.2.2.5 Government grants and accounting requirements

34.15.2.2.5.1 Overview

As per Section Section 34.64 of FRS 102 the accounting for government grants should follow the guidance in Section 24 of FRS 102. Such grants can be accounted for under the accruals model or the performance model (note SORP only permits the performance model however FRS 102 permits both). See further details at 24.3.2 and 24.4.2 in Section 24.

34.15.2.2.5.1.1 Grants of all natures (including optional grants) – Performance model

NOTE FULL FRS 102 SORP ONLY PERMITS THE PERFORMANCE MODEL TO BE UTILISED FOR GRANTS. FRS 102 GIVES A CHOICE TO EITHER APPLY THE PERFORMANCE MODEL OR THE ACCRUALS MODEL

Grants of all natures (including capital grants) – note change here from full FRS 102

a) If there are no performance conditions attached then recognise (ignore restriction on how the funds are to be used)

– Immediately assuming the charity has:

– Entitlement

– Probable economic benefits will flow

– Can be reliably measured

– Even if costs have not been incurred the income must be recognised in the SOFA (applies to capital grants also)

– If there are performance conditions attached then recognise:

– Only when the performance conditions are met

– Even if costs have not been incurred the income must be recognised in the SOFA (applies to capital grants also)

b) Example of performance conditions:

-

- service level conditions, or

- a set number of output to be done, or

- opening hours of facilities, or

- number of meals to be provided

- Requirement to employ a certain number of staff for a set period

c) Terms attaching to a grant which can be ignored when looking if the performance conditions have been met:

- Rules restricting the use of the funds

- Conditions that allow for the recovery of the grant by the donor of any unexpended part of a grant:

- Terms which are within the charity’s control & there is sufficient evidence that the terms will be met. Examples include:

- Submission of accounts or certification of expenditure

- The requirement to hold it for charitable purposes and if sold to invest in charitable activities (as this is stated in the charity constitution then this is a given)

d) Accruals model with regard to government grants cannot be used under FRS 102 SORP (however it can be used if FRS 102 non SORP accounts are being prepared).

- Must be recognised in income when performance conditions are met (regardless if costs have not been incurred).

34.15.2.2.5.1.2 Accrual model FRS 102 only (cannot be utilised under SORP FRS 102):

the accruals model recognises the grant so as to match it with the costs incurred. So for revenue type grants such as training grants, the grant could be recognised in income in any of the following ways:

– Matched against direct training costs

– Taken over a period of time against salary for the employees expected to benefit from the training

– Taken systematically over a straight line basis

– Taken when cash is received

As can be seen there will be judgement required as to which best meets the company requirements. It is vital that the company applies the policy chosen consistently and discloses this in the accounting policies.

34.15.2.2.5.2 Example of government grant accounting of PBE’S

Example 23: Accruals model – capital grant – depreciable asset (applicable for FRS 102 only and not Charities SORP)

Charity A received a grant of CU100,000 towards the cost of constructing its premises for provision of its charitable activities. This grant was provided on condition that the charity construct a specialist treatment unit for a certain type of beneficiary a number of years ago and on condition that it continue to be used by the charity for that purpose and if it is sold the disposals proceeds must be utilised for charitable purposes.

The useful life of the premises itself is 50 years.

In this case, the amount to be recognised each year will be based on the 50 year life as this is the life that the asset is depreciated over. Hence there is a matching of the depreciation charge on the property with amortisation of the grant. The total grant to be released each year is CU2,000 (CU100,000/50yrs). The journals required are:

| CU | CU | |

| Dr Bank | 100,000 | |

| Cr Deferred Revenue/Grant Liability | 100,000 |

Being journal to recognise receipt of the funds

| CU | CU | |

| Dr Accumulated Amortisation on Grant Liability | 2,000 | |

| Cr Grant Amortisation – Other income | 2,000 |

Being journal to recognise the release of the grant each year for 50 years.

If the above was a grant on land, which is non-depreciable, it is likely that this should be released over the terms of the building constructed on it.

Example 24: Accruals model (applicable for FRS 102 only and not Charities SORP) – capital grant

Charity A received a grant of CU100,000 towards the cost of constructing its premises. A condition of the grant is that the Charity continues to utilise the manufacturing plant for a period of 20 years. As part of the grant they are required to maintain employment for 3 years.

In this particular case, judgement will have to be made as to whether in substance this is a capital grant or a revenue grant. All facts would have to be reviewed. However, given the large grant and the fact that it is principally towards the cost of the plant, in this particular case it would be treated as a capital grant and accounted for accordingly.

Example 25: Accruals model (applicable for FRS 102 only and not Charities SORP) – revenue grant

If in example 23, the above was a Capital Assistance Scheme loan from a local authority to purchase a property to be used to house beneficiaries of the charity. This loan is mortgaged on the property. As part of the loan the charity is required to keep the properties in good structural order and proper repair and ensure that they are used for the charities purpose and let to eligible persons and rented to beneficiaries at fair rates. If the above conditions are met the loan will be forgiven after 20 years of receipt. If repayment is not made if requested the provider can take steps to recover the loan through the mortgage held.

In this case the loan is considered government assistance. The journals required under the accruals model would be the same as above.

Note if this was a Capital Assistance loan which was not from a government agency it would be accounted as a concessionary loan under Section 11 of FRS 102 – the journals would differ as the loan would remain at 100k for the 20 years until forgiven.

Example 26: Accruals model (applicable for FRS 102 only and not Charities SORP) – revenue grant

Charity A obtained a grant for the cost of carrying out research which will go on for three years. The total amount of the grant was CU100,000. It was conditional on using the funds for this service and no other conditions were imposed. The costs are expected to incurred over the 3 year life evenly. Under the accruals model the income would be recognised evenly over a 3 year period (i.e. CU33,333 per annum). The journals required are to:

| CU | CU | |

| Dr Bank | 100,000 | |

| Cr Deferred revenue | 66,667 | |

| Cr Income in P&L/I&E | 33,333 |

Example 27: Performance model (applicable for FRS 102 and Charities SORP) – revenue grant

Charity A obtained a grant for the cost of carrying out research which will go on for three years. The total amount of the grant was CU100,000. It was conditional on using the funds for this service and no other conditions were imposed. The costs are expected to incurred over the 3 year life evenly. As it is probable that the conditions for this grant will be met (which are within the control of the charity), and given that there are no other performance conditions, under the performance model the full grant should be recognised in income on receipt.

The journals required are to:

| CU | CU | |

| Dr Bank | 100,000 | |

| Cr Donations in SOFA OR Income in P&L/I&E | 100,000 |

Example 28: Performance model – Revenue Grant

Charity A received a Capital Assistance Scheme loan of CU100,000 from a local authority to purchase a property to be used to house beneficiaries of the charity. This loan is mortgaged on the property. As part of the loan the charity is required to keep the properties in good structural order and proper repair and ensure that they are used for the charities purpose and let to eligible persons and rented to beneficiaries at fair rates. If the above conditions are met the loan will be forgiven after 20 years of receipt. If repayment is not made if requested the provider can take steps to recover the loan through the mortgage held.

As these are loans which are considered repayable unless certain conditions are met, it comes within the remit of Section 5 of SORP. As the charity must maintain the property to certain conditions and ensure they are let to eligible persons at a fair rate these would reflect performance conditions. Therefore the loan cannot be released to income until the 20 year period is over and all of the performance conditions have been met. This loan would be shown as a creditor greater than one year and only released as a donation on the expiry of the 20 years assuming all the conditions are met. This is supported by Section 11 of FRS 102 & Section 11 of SORP which specifically states that a liability cannot be derecognised until there is formal forgiveness of the loan received.

The journals required on initial receipt are:

| CU | CU | |

| Dr Bank | 100,000 | |

| Cr Government Capital Assistance loans – Loans > 1 year | 100,000 | |

| Being journal to defer income on initial recognition | ||

The journals required on expiry of 20 years

| CU | CU | |

| Dr Loans in ‘creditors: amounts falling due within one year’ | 100,000 | |

| Cr Donations & Legacies – unrestricted fund in SOFA OR Income in I&E/P&L | 100,000 | |

| Being journal to release the loan once it has been forgiven | ||

Note if this was a loan which was not from a government agency it would be accounted as a concessionary loan – the journals would remain the same.

Example 29: Capital grants (FRS 102 and FRS 102 SORP – performance model)

Assume that a capital grant has been received by the charity in the year of CU50,000. The conditions of the grant states that the grant is conditional on the charity providing 100% occupancy for five years with the amount reducing for each of these 5 years.

Assume the 100% occupancy was achieved in year one.

Under this method the following would be the journals under the performance model:

| CU | CU | |

| Dr bank | 50,000 | |

| Cr income from charitable activities – restricted fund or turnover in P&L/I&E (CU50,000/5 yrs* 1 yr gone) | 10,000 | |

| Cr deferred revenue | 40,000 | |

| Being journal to defer the amount over the 5 year period | ||

If the condition of the grant stated that the full amount of the grant is repayable if the 5 year condition is not met, then no income would be recognised until the end of year 5.

Example 30: Grants and performance conditions

A grant was to be provided to a charity subject to the Charity obtaining matching funds to allow the construction to be completed. Given that this is a performance related condition the grant cannot be recognised in income until the matching funding is obtained by the charity. The journal to defer would be to Dr Bank and Cr Deferred revenue.

Example 31: Grants and performance conditions

A grant was to be provided to a charity subject to the Charity obtaining planning permission to allow the construction to be completed. Given that this is a performance related condition the grant cannot be recognised in income until planning permission is obtained by the charity.

Example 32: Grants and performance conditions

A grant was provided by the HSE to a charity on condition that a certain service level must be achieved throughout the year. Given that this is a performance related condition the grant cannot be recognised in income until the service conditions have been met.

Example 33: Grants and performance conditions

A grant is provided subject to the charity providing a number of work placements in a particular period. In this case the income can only be recognised in the specified period in which the work placements are completed (i.e. the grants restricts when the work placements can be given). In this case the grant would be deferred until this period has elapsed and the requirements have been met.

This is similar where a number of training weeks are specified as part of the grant.

Example 34: Grants and performance conditions

A multi-period grant has been approved for a charity. However it will only be paid on the basis of agreed budgets. On this basis the charity cannot recognise the income until the grant provider has approved the budgets.

[/et_pb_text][/et_pb_column][et_pb_column type=”1_4″][et_pb_toggle _builder_version=”3.0.106″ title=”Practical Examples” open=”off”]

Examples

Example 2: Application of the fair value model com.

Example 3: Application of the fair value model – livestock.

Example 4: Biological Assets held at fair value.

Example 5: Extract from notes to the financial statements for biological assets held at fair value.

Example 6: Extract from accounting policies notes for livestock/biological assets carried at cost.

Example 14: Donated goods or services – fixed assets.

Example 15: Donated goods or services – donated goods held for resale – impractical to measure.

Example 16: Donated goods or services – donated goods held for resale – practical to measure.

Example 18: Donated goods or services – donated services.

Example 19: Business Combinations: Gifts of business etc.

Example 20: Business Combinations: Mergers.

Example 21: Concessionary loans – option not to discount.

Example 22: Concessionary loans – option to discount.

Example 24: Accruals model (applicable for FRS 102 only and not Charities SORP) – capital grant.

Example 25: Accruals model (applicable for FRS 102 only and not Charities SORP) – revenue grant.

Example 26: Accruals model (applicable for FRS 102 only and not Charities SORP) – revenue grant.

Example 27: Performance model (applicable for FRS 102 and Charities SORP) – revenue grant.

Example 28: Performance model – Revenue Grant.

Example 29: Capital grants (FRS 102 and FRS 102 SORP – performance model).

Example 30: Grants and performance conditions.

Example 31: Grants and performance conditions.

Example 32: Grants and performance conditions.

Example 33: Grants and performance conditions.

Example 34: Grants and performance conditions.

[/et_pb_toggle][/et_pb_column][/et_pb_row][/et_pb_section]