[et_pb_section admin_label=”Header – All Pages” global_module=”1221″ transparent_background=”off” background_color=”#1e73be” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”||0px|”][et_pb_row global_parent=”1221″ admin_label=”row”][et_pb_column type=”4_4″][et_pb_post_title global_parent=”1221″ admin_label=”Post Title” title=”on” meta=”off” author=”on” date=”on” categories=”on” comments=”on” featured_image=”off” featured_placement=”below” parallax_effect=”on” parallax_method=”on” text_orientation=”left” text_color=”light” text_background=”off” text_bg_color=”rgba(255,255,255,0.9)” module_bg_color=”rgba(255,255,255,0)” title_all_caps=”off” use_border_color=”off” border_color=”#ffffff” border_style=”solid” title_font=”|on|||” title_font_size=”35″ custom_padding=”10px|||”] [/et_pb_post_title][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” global_module=”1228″ fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” custom_padding=”0px||0px|” padding_mobile=”on” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row global_parent=”1228″ admin_label=”Row” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” use_custom_gutter=”off” gutter_width=”3″ custom_padding=”0px||0px|” padding_mobile=”off” allow_player_pause=”off” parallax=”off” parallax_method=”off” make_equal=”off” parallax_1=”off” parallax_method_1=”off” column_padding_mobile=”on”][et_pb_column type=”4_4″][et_pb_text global_parent=”1228″ admin_label=”Text” background_layout=”light” text_orientation=”left” text_font_size=”14″ use_border_color=”off” border_color=”#ffffff” border_style=”solid”]

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” fullwidth=”off” specialty=”off”][et_pb_row admin_label=”Row”][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” text_font_size=”14″ use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”http://www.frs102.com/members/premium-toolkit/” type=”big” color=”red”] Return to Main Index[/button] [/et_pb_text][/et_pb_column][et_pb_column type=”1_2″][et_pb_text admin_label=”Text” background_layout=”light” text_orientation=”center” text_font_size=”14″ use_border_color=”off” border_color=”#ffffff” border_style=”solid”] [button link=”http://frs102.com/members/premium-toolkit/section-11/” type=”big” color=”red”] Return to Section 11 Home[/button] [/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section][et_pb_section admin_label=”Section” fullwidth=”off” specialty=”off” transparent_background=”off” allow_player_pause=”off” inner_shadow=”off” parallax=”off” parallax_method=”off” padding_mobile=”off” make_fullwidth=”off” use_custom_width=”off” width_unit=”on” make_equal=”off” use_custom_gutter=”off” gutter_width=”3″][et_pb_row admin_label=”Row”][et_pb_column type=”4_4″][et_pb_text admin_label=”Main Body Text” background_layout=”light” text_orientation=”justified” use_border_color=”off” border_color=”#ffffff” border_style=”solid”]Presentation

Extract from FRS 102 Section 11.38A

11.38A A financial asset and a financial liability shall be offset and the net amount presented in the statement of financial position when and only when, an entity:

(a) currently has a legally enforceable right to set off the recognised amounts; and

(b) intends either to settle on a net basis, or to realise the asset and settle the liability simultaneously.

OmniPro comment

Unless there is a legal entitlement there is no right of set off. Therefore for example a invoice discounting facility with recourse, the liability in relation to fund advanced from the bank cannot be set against the trade debtor balance.

For derivatives dealt with under Section 12, the fair value loss and profits of forward contracts/interest rate swap cannot be set against each other. They must be classified within assets and liabilities.

Principal transition adjustments

OmniPro comment

- Under old GAAP, there was no requirement to carry the financial assets or liabilities at amortised cost. Therefore, on transition for financial assets and liabilities which were not derecognised under old GAAP, an entity will have to identify financial assets and liabilities where there is a financing transaction (i.e. a loan advanced/received at favourable rates and is not repayable on demand) and then determine the market rate on such loans at the date of drawdown/advancement. Then determination has to be made as to the amortised cost to be recognised on transition. For intercompany loans, there may be tax implications for these adjustments where the disregard provisions are not applied.

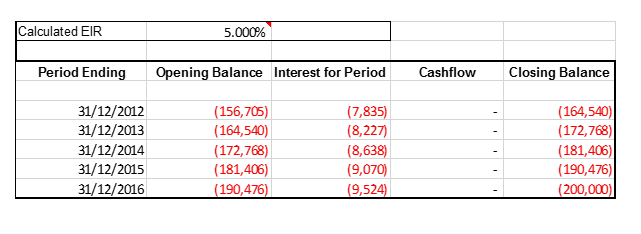

Example 26: Loans at non-market rates on transition

Company A is a subsidiary of Parent B. Parent B provides a loan to Company A for 5 years for CU200,000 on 01/01/2012. No interest is charged on the amount loaned. The market rate of interest that would have been charged on this loan by a third party on 01/01/13 i.e. a bank would be 5%. The date of transition is deemed to be 01/01/14. The carrying amount of the loan in the subsidiary and parent financial statements under old GAAP at 01/01/14 was CU200,000 as there was no requirement to account for the loan based on its present value of future cash flows. Assume the adjustments are not taxable/tax deductible under tax legislation rules and there are no transfer pricing adjustments required.

Given that a financing arrangement exists, there is a need to determine the present value of the future payments using the inputted market rate. Therefore amount to be recognised initially is:

CU200,000 / (1.05)^5 = CU156,705

The difference between CU200,000 and CU156,705 is in effect a deemed gift from the parent for the fact that the loan was given interest free.

The transition adjustments to the opening balance sheet at 01/01/14 are as follows:

In the subsidiary financial statements

| CU | CU | |

| Dr Intercompany Loan (CU200,000 – CU172,768 being the required carrying amount at date of transition) | 27,232 | |

| Dr Profit and Loss Reserves (i.e. 2012 and 2013 interest charge) | 16,063 | |

| Cr Capital Contribution (CU200,000-CU156,705 being the PV on future payments on inception of the loan) | 43,295 |

Being journal to show the correct amortised cost at the date of transition and the initial capital contribution received

In the parent financial statements

| CU | CU | |

| Dr Investment in Company A (CU200,000-CU156,705 being the PV on future receipts on inception of the loan) | 43,295 | |

| Cr Intercompany Loan Receivable | 27,232 | |

| Cr Profit and Loss Reserves (i.e. 2012 and 2013 interest income) | 16,063 |

Being journal to show the correct amortised cost at the date of transition

The adjustments required to adjust the comparative year (year ended 31/12/14) assuming the opening transition journals above are carried forward and P&L journals above posted to reserves:

In the subsidiary financial statements

| CU | CU | |

| Dr Interest Expense | 8,638 | |

| Cr Intercompany Loan | 8,638 |

Being journal to reflect the deemed interest charge for the 31/12/14 period as per the calculation above

In the parent financial statements

| CU | CU | |

| Dr Intercompany Loan | 8,638 | |

| Cr Interest Income | 8,638 |

Being journal to reflect the deemed interest income for the 2014 year as per the calculation above

The adjustments required to adjust the current year (year ended 31/12/15) assuming the opening transition journals above and the 2014 journals are carried forward and P&L journals above posted to reserves:

In the subsidiary financial statements

| CU | CU | |

| Dr Interest Expense | 9,070 | |

| Cr Intercompany Loan | 9,070 |

Being journal to reflect the deemed interest charge for the 31/12/15 period as per the calculation above

In the parent financial statements

| CU | CU | |

| Dr Intercompany Loan | 9,070 | |

| Cr Interest Income | 9,070 |

Example 26a: Directors loan at non-market rates on transition

If we take example 26 above and this time assume the loan was provided to Company A by its director/shareholder. Assume the adjustments are taxable/ tax deductible under UK tax law and therefore deferred tax is required to be recognised on transition. Assume a deferred tax rate of 10% and the tax transition adjustments will be taxable/tax deductible over a 10 year period from 2015 on.

The transition adjustments to the opening balance sheet at 01/01/14 would be as follows:

In the Company A financial statements

| CU | CU | |

| Dr directors loan (200,000 – 172,768) | 27,232 | |

| Cr profit and loss reserves | 27,232 |

| CU | CU | |

| Dr Profit and Loss reserves with deferred tax (CU27,232*10%) | 2,723 | |

| Cr Deferred Tax Liability | 2,723 |

Being journal required to reflect the correct amortised cost on transition and the related deferred tax impact. This goes to profit and loss reserves as initially the difference between the present value and the carrying amount would be posted to interest income

The journals mentioned above for the subsidiary are relevant here for the 2014 and 2015 year but deffered tax would need to be considered in the example for end of year.

Additional deferred tax journals to be posted in 2014 are:

| CU | CU | |

| Dr Deferred Tax Liability (CU8,638*10%) | 864 | |

| Cr Deferred Tax in P&L | 864 |

Being journal to reflect the release of deferred tax for the additional not and interest charged in 2014.

Additional deferred tax journals to be posted in 2015 are:

| CU | CU | |

| Dr deferred tax liability (1859/10 years) | 186* | |

| Cr deferred tax in P&L | 186 |

Being journal to release 1/10th of the deferred tax liability of CU1859.

*Total carrying amount of deferred tax liability at 31/12/14 of CU1,859 (CU2,732 – CU864) divided by 10 years being the assumed period in which this transition adjustment will be included in the tax computation for taxation purposes (i.e. CU18,594 (CU27,232 – CU8638) divided by 10 years = CU1,859 which will be taxed at 10% in the 2015 year assuming a tax rate of 10%. For 9 years after 2015 the same deferred tax journal of CU186 will be required so as to match the amount taxed in the tax computation on the transition adjustment.

Example 26b: Related party company loan at non-market rates on transition

If we take example 26 above and this time assume the loan was provided to Company A by a related company, Company B.

The transition adjustments to the opening balance sheet at 01/01/14 would be as follows:

In the Company A financial statements

| CU | CU | |

| Debit intercompany loan (CU200,000 – CU172,768) | 27,232 | |

| Credit profit and loss reserves | 27,232 |

Being journal required to reflect the correct amortised cost on transition. This goes to profit and loss reserves as initially the difference between the present value and the carrying amount would be posted to interest income

The journals mentioned in example 26 above for the subsidiary are relevant here for the 2014 and 2015 year. There is no deferred tax impact as it is from a corrected company therefore the adjustments are not taxable/tax deductible.

Example 26c: Directors loan at non-market rates on transition

If we take example 26 above and this time assume that Company A provided a loan to its directors for the same amount.

The transition adjustments to the opening balance sheet at 01/01/14 would be as follows:

In the Company A financial statements

| CU | CU | |

| Debit profit and loss reserves | 27,232 | |

| Credit directors loan (CU200,000 – CU172,768) | 27,232 |

Being journal required to reflect the correct amortised cost on transition. This goes to profit and loss reserves as initially the difference between the present value and the carrying amount would be posted to interest expense. Note if the loan was provided to a shareholder, then there could be an argument for this to be posted to other reserves in equity.

The journals mentioned above for the subsidiary are relevant here for the 2014 and 2015 year.

There is no deferred tax impact as it is from a corrected company therefore the adjustments are not taxable/tax deductible

2. Investment in non-puttable ordinary and preference shares to be recognised at fair value

Under Section 11 where the investments are listed on the stock exchange or where other non-listed investments can be reliably measured, these should be accounted for at fair value on transition. Under old GAAP it is likely that these were carried at cost less impairment. The uplift in fair value will need to be recognised in reserves at the date of transition. Deferred tax will also need to be recognised on this uplift at the sales tax rate (CGT rate).

Example 27: Non-puttable ordinary shares at market value

Company A had an investment in ordinary shares which were list on the stock exchange. If we assume the date of transition is 01/01/14 and the market value of these shares at that date was CU10,000. Under old GAAP the carrying amount of these shares was CU6,000 being their original cost. Assume the deferred tax rate is 20% (CGT rate). The fair value at 31/12/14 was CU11,000 and CU9,000 at 31/12/15.

The transition adjustments required to adjust the opening balance sheet at 01/01/14 are:

| CU | CU | |

| Dr Investments at Fair Value | 4,000 | |

| Cr Profit and Loss Reserves (CU10,000 – CU6,000 cost) | 4,000 | |

| Dr Profit and Loss Reserves for Deferred Tax (CU4,000*20%) | 800 | |

| Cr Deferred Tax Liability | 800 |

Being journal to reflect the fair value at the date of transition and the related deferred tax on the uplift.

The adjustments required to adjust the comparative year (year ended 31/12/14) assuming the opening transition journals above are carried forward and P&L journals above posted to reserves

| CU | CU | |

| Dr Investments at Fair Value | 1,000 | |

| Cr Profit and Loss – Finance Income (CU11,000 – CU10,000 prior carrying amount) | 1,000 | |

| Dr Deferred Tax in P&L (CU1,000*20%) | 200 | |

| Cr Deferred Tax Liability | 200 |

Being journal to reflect the movement in fair value during the year and the related movement on deferred tax

The adjustments required to adjust the current year (year ended 31/12/15) assuming the opening transition journals above and the 2014 journals are carried forward and P&L journals above posted to reserves:

| CU | CU | |

| Dr Profit and loss – Finance Expense (CU11,000 prior carrying amount – CU9,000) | 2,000 | |

| Cr Investments at Fair Value | 2,000 | |

| Dr Deferred Tax Liability | 400 | |

| Cr Deferred Tax in P&L (CU2,000*20%) | 400 |

Being journal to reflect the movement in fair value during the year and the related movement on deferred tax

- A sale with unusual credit terms (not normal credit terms) and is therefore deemed a financing transaction

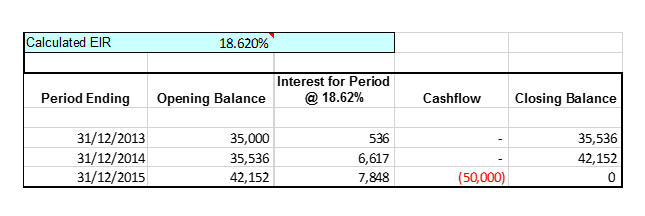

Under Section 11, where a financing transaction is included within a sale, the amount to be recognised within revenue is the cash price that would be charged where no unusual credit terms were provided. The deemed financing element is posted as interest/finance income in the P&L and released over the terms of the credit provided. Deferred tax will need to be recognised on transition in the opening balance sheet and assume it will be reversed over the financing period. Under old GAAP, this sale was recognised at the gross amount and not present valued (i.e. sale recognised for CU50,000).

Example 28: Sale with unusual credit terms

Company A sold goods worth CU50,000 with unusual credit terms on 01/12/13 (date of transition is 01/01/14 as in the example above). The credit provided is for a period of up to 31/12/15. The normal cash price for these goods would be CU35,000. Under old GAAP CU50,000 was recognised in 2013 and the carrying amount in debtors at 01/01/14 was CU50,000. The difference of CU15,000 is determined to be a financing transaction. Assume the deferred tax rate is 10%. The effective interest rate is calculated at 18.62% as per below. The effective interest rate is determined so as to write the deemed interest into the P&L over the life of the transaction. The effective interest rate is determined through trial and error or through the use of excel.

The transition adjustments required to adjust the opening balance sheet at 01/01/14 are:

| CU | CU | |

| Dr Profit and Loss Reserves (CU15,000-CU536 which relates to pre transition) | 14,464 | |

| Cr Trade Debtors | 14,464 | |

| Dr Deferred Tax on BS (CU14,464*10%) | 1,446 | |

| Cr Profit and Loss Reserves for Deferred Tax | 1,446 |

Being journal to reflect correct carrying amount of CU35,536 in the opening balance sheet and the effect of deferred tax on this adjustment (deferred tax as this was taxed under old GAAP but it has not hit the profit and loss account under FRS 102 at this time, so assumed the assumed deferred tax will be released as this is released to the profit and loss as this amount will be deducted in the tax computation going forward)

The adjustments required to adjust the comparative year (year ended 31/12/14) assuming the opening transition journals above are carried forward and P&L journals above posted to reserves.

| CU | CU | |

| Dr Trade Debtors | 6,617 | |

| Cr Finance Income in P&L (so that the carrying amount is now CU42,152) | 6,617 | |

| DR Deferred Tax P&L | 661 | |

| Cr Deferred Tax on BS (CU6,617*10%) | 661 |

Being journal reflect the deemed interest income in the profit and loss for the year and the related deferred tax effect

The adjustments required to adjust the current year (year ended 31/12/15) assuming the opening transition and 2014 journals above are carried forward to reserves.

| CU | CU | |

| DR Trade Debtors | 7,848 | |

| Cr Finance Income in P&L (so that the carrying amount is now CU50,000) | 7,848 | |

| Debit Deferred Tax P&L | 785 | |

| Cr Deferred Tax on BS (CU7,848*10%) | 785 |

Being journal reflect the deemed interest income in the profit and loss for the year and the reversal of the related deferred tax for the fact that this will be taxable in the tax computation in the current year.

Example 28a: Purchase with unusual credit terms

If we took example 28 above and assume that Company B was the purchaser. The journals required would be as follows:

The transition adjustments required to adjust the opening balance sheet at 01/01/14 are:

| CU | CU | |

| Dr Trade Creditors | 14,464 | |

| Cr Profit and Loss Reserves (CU15,000-CU536 which relates to pre transition) | 14,464 | |

| Dr Profit and Loss Reserves for Deferred Tax | 1,446 | |

| Cr Deferred Tax on BS (CU14,464*10%) | 1,446 |

Being journal to reflect correct carrying amount of CU35,536 in the opening balance sheet and the effect of deferred tax on this adjustment (deferred tax as a tax deduction was claimed under old GAAP but it has not hit the profit and loss account under FRS 102 at this time, so the deferred tax will be released as this is released to the profit and loss as this amount will be added back in the tax computation going forward)

The adjustments required to adjust the comparative year (year ended 31/12/14) assuming the opening transition journals above are carried forward and P&L journals above posted to reserves.

| CU | CU | |

| Dr Finance Expense in P&L (so that the carrying amount is now CU42,152) | 6,617 | |

| Cr Trade Creditors | 6,617 | |

| Dr Deferred Tax on BS (CU6,617*10%) | 661 | |

| Cr Deferred Tax P&L | 661 |

Being journal reflect the deemed interest income in the profit and loss for the year and the related deferred tax effect

The adjustments required to adjust the current year (year ended 31/12/15) assuming the opening transition and 2014 journals above are carried forward to reserves.

| CU | CU | |

| Dr Finance Expense in P&L (so that the carrying amount is now CU50,000) | CU7,848 | |

| Cr Trade Creditors | CU7,848 | |

| Dr Deferred Tax on BS (CU7,848*10%) | CU785 | |

| Cr Deferred Tax P&L | CU785 |

Being journal reflect the deemed interest income in the profit and loss for the year and the related deferred tax effect

Transition exemptions contained with FRS 102

Section 35.9 states that a financial asset or liability previously derecognised under old GAAP cannot be recognised under FRS 102 on transition. In addition, if there are financial assets or liabilities that would have been derecognised under FRS 102 but are still recognised under old GAAP, entities have a choice to either derecognise on transition or continue until it is settled.

Under Section 35.10 a substantial modification which occurred pre transition but was not treated as an extinguishment under old GAAP does not need to be accounted for on transition instead the new modified financial liability can be recognised at the date of transition.

The exemption mentioned below (Section 35.10(u) & (v) cannot be chosen by Republic of Ireland companies at this time as the EU Directive 2013/34 has not been enacted. This is expected to be enacted in early 2016.

Section 35.10(u-v) exemptions allow a small entity to:

- Not restate the comparative figures disclosed in the first set of financial statements prepared under FRS 102 for the following:

(For example, assume Company A has a year end of 31 December. The date of transition would then be 1 January 2014 and the comparatives would be for the year ended 31 December 2014. In this case the 2014 comparatives would not need to be adjusted)

- Financial instruments required to be held at fair value under Section 11 and Section 12 of FRS 102. Examples of what would need to be fair valued under these sections are:

- Fair valuing forward foreign exchange contracts

- Fair valuing interest rate swaps

- Investments where the entity does not hold a significant influence (usually less than 20% owned) which can be measured reliably (i.e. publically traded shares

- Sales and purchases to/from related parties (as defined in Section 33) where payment is beyond normal business terms

- Loan to/from related parties which are at non-market rates.

The small entity will measure the above assets/liabilities in line with the accounting policy adopted under old GAAP.

Where this exemption is claimed the small entity will post the carrying amount through the current year by posting it to opening retained earnings. When measuring the assets/liabilities at that date a small company can determine the market rates on the loan based on a market rate at that date. There is no requirement to try to determine these rates at the time the loan was initially entered into.

[/et_pb_text][/et_pb_column][/et_pb_row][/et_pb_section]